Over the past five years, interest rates have edged higher and fluctuated from month to month, leading bankers across the Granite State to balance risk with continued lending that helps businesses and individuals invest in their future. This could mean adjusting loan structures for a business or focusing on more affordable housing options like manufactured homes and accessory dwelling units (ADUs).

As the economy has been shaken by government shutdowns and reorganizations, tariffs and now a war in the Middle East, bankers say the environment is increasingly difficult to predict. That uncertainty is compounded by the pace and volatility of interest rate changes, according to Christopher Logan, president and CEO of Bank of NH and vice chair of the NH Bankers Association, who says the current environment is unlike anything he has seen in decades of banking.

“It seems like it’s changing faster today and with more wild swings than ever,” Logan says. “Ninety days ago, there was talk of rate cuts. Now it’s no cuts and some are even talking about increases. Ninety days from now, it could be a completely different conversation.”

For community banks, those abrupt changes carry outsized consequences. Logan notes that roughly 80% of a community bank’s revenue is derived from interest income—the spread between loans and deposits—compared to closer to 50% for larger national or regional banks that rely more heavily on fee-based services. That makes community institutions particularly sensitive to rapid rate movements.

“If rates move in an organized fashion, it’s manageable,” he says. “It’s when there’s a hockey stick increase or decrease. That creates real pressure on margins and balance sheets.”

From a business perspective, rising rates tend to shift focus toward efficiency and cash flow. “A loan you might have gotten at 3%, you might not get if it jumps to 6%,” says Adam Hamilton, a senior business development officer at Claremont Savings Bank.

“Now the emphasis shifts to whether the business can consistently generate the cash flow to support the debt.”

Shifts like this have direct implications for underwriting, which can affect the ability of small businesses and communities to thrive. As rates increase, banks apply greater scrutiny and allow less flexibility, particularly for deals that may have been marginal in a lower-rate environment. Logan adds that while data and analytics continue to grow in importance, traditional lending fundamentals still play a critical role.

“There’s still the five C’s of credit, and one of those is character,” he says. “If something is on the margin, that can push a decision one way or the other. That’s where community banks have an advantage. We’re local, we know our customers, and we understand their track records.”

“If cash flow is already tight and rates go up, that introduces more risk for both the business and the bank,” Hamilton adds. “At the end of the day, the goal isn’t to take control of assets, it’s to structure something that gets repaid.”

This sentiment is equally true for lenders who serve those with fewer resources and less access to the banking system. Steve Saltzman, CEO of the NH Community Loan Fund, says when rates rise it affects everything. “It impacts debt-to-income ratios, cash flow, and ultimately whether a project is feasible,”

he says.

For small businesses and nonprofits, higher borrowing costs can delay or shrink projects. “They may need to bring more equity to the table, or scale something back,” Saltzman says. “Sometimes projects just don’t happen.”

Josephine Moran, president and CEO of Ledyard Bank in Hanover, sees that same dynamic playing out across her institution’s portfolio. “Interest rates affect cash flow, and cash flow affects small businesses’ flexibility and resilience,” she says. “But every business is different. There’s no cookie-cutter resolution.”

Factors Affecting Lending

For businesses across NH, interest rates are just one factor shaping the lending landscape, says John Bortolotto, senior vice president and commercial loan officer at Mascoma Bank, with branches throughout the Upper Valley. “Interest rates are just one sliver of the overall pie,” he says.

Hamilton says interest rates matter less as a static number than as a catalyst for behavioral change. “It’s not always so much whether rates are higher or lower,” Hamilton says. “When rates change, that changes behavior.”

When behavior shifts, driven by interest rates as well as pressures like workforce constraints and the lack of affordable housing, local businesses and communities feel the impact. Logan emphasizes that access to capital for small businesses remains essential to the state’s economic health, particularly in a state where local enterprises drive job creation, wage growth and tax revenue.

“Access to capital for small businesses is really important for our state,” Logan says. “That’s where GDP growth comes from, that’s where wage growth comes from, that’s where jobs come from.”

That dynamic underscores the continued importance of community banking, where deposits are recycled back into the local economy. The NH Bankers Association and the FDIC reported late last year that the Granite State reinvests deposits in local communities at the highest rate in the nation.

But Logan cautions that this reinvestment model—central to how economic development has functioned for generations—is facing new pressures.

“Economic development has always worked because banks take deposits and re-lend them back into the community,” he says. “That’s how people get houses, how businesses expand, how jobs are created.”

Increasingly, however, those deposits may not remain in the traditional banking system. Logan points to the growth of out-of-market national institutions, financial technology firms and emerging instruments such as cryptocurrency and stablecoins as potential disruptors.

“If those dollars start leaving the banking system—whether its to an out-of-market bank, an offshore institution or crypto—you have to ask what happens to lending,” he says. “If Walmart or another company gets your dollars, they’re not reinvesting them back into Laconia, New Hampshire. They’re reinvesting them back into their own business.”

For Logan, that collaborative, locally rooted model is what is at stake in a rapidly evolving financial landscape. Where individuals and businesses choose to bank, he says, has direct consequences for the strength of local economies. “That’s a big question mark for me,” he says. “It’s something we need to be thinking about more.”

Moran, who relocated to NH in 2022 after a leadership role at Provident Bank in New Jersey, now oversees a $1 billion bank with a $2.3 billion wealth business at Ledyard, serving more than 4,000 business clients across NH, Vermont and southern Maine. Ledyard has expanded its footprint beyond the Upper Valley and New London to Concord and Bedford while maintaining a high-touch, community banking model.

She says short-term rates influence how businesses operate today, while long-term rates shape future planning. But access to capital ultimately depends on a broader financial picture.

“We’re here to help people solve their needs,” Moran says. “Even in a higher-rate environment, we’ll look at the full picture and that includes cash flow, growth potential, and how to structure a solution that works.”

That might mean extending amortization periods from 20 to 30 years, adjusting loan structures or helping clients think strategically about revenue growth. “Are they maximizing revenue? Can we help them grow?” she says. “That leads to stronger cash flow, which supports lending.”

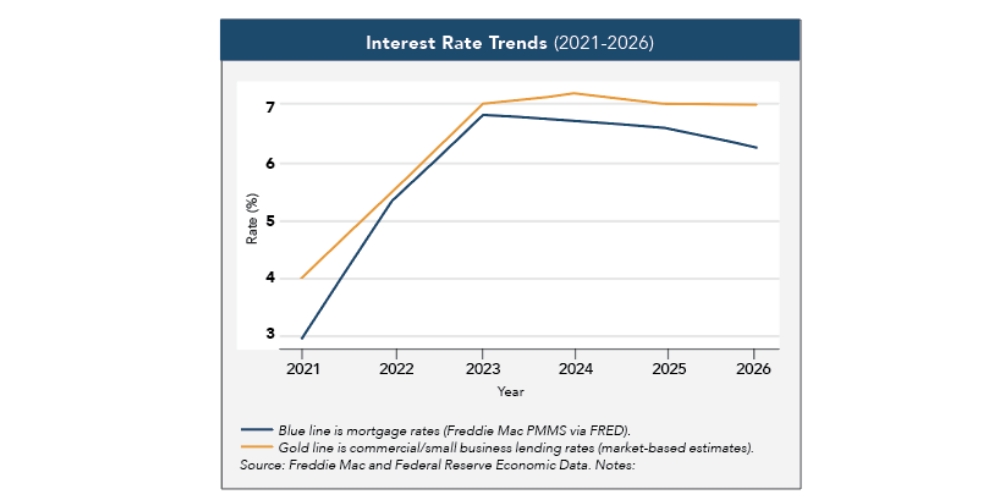

Looking back over the past 20 years, Bortolotto explains that borrowing conditions have moved through dramatic cycles. Rates climbed to roughly 8.5% to 9% ahead of the 2006–2007 financial crisis, then dropped sharply and remained low for years. During the COVID-19 pandemic, rates fell to historic lows near 3%, before rising again as the Federal Reserve sought to curb inflation.

Mortgage rates, according to Freddie Mac, hovered around 6.3% at the end of March for 30-year fixed-rate loans, while commercial lending rates for business borrowing averaged closer to 6.9%, based on industry reporting. A year ago the 30-year fixed-rate mortgage averaged 6.65%. Those figures sit near the midpoint of the past two decades, but structural constraints like workforce shortages, energy costs and housing availability have changed dramatically, Bortolotto notes. “Today’s rates are somewhere in the middle,” he says, “but everything else around them is very different.”

Individual Approach is Critical

Bortolotto, who specializes in commercial lending at Mascoma Bank, says lending is both project-specific and company-specific.“You’re really looking at the borrower’s ability to pay from the cash that’s generated,” he says. “But you also have to understand risk. If just one or two clients represent a meaningful percentage of your revenue, that’s a different conversation.”

Service-based businesses such as consultants, healthcare providers or accounting firms may generate strong revenue but lack physical assets to secure a loan, requiring a more nuanced approach.

Hamilton, who operates a business as well as financing them, says that dual perspective is critical. “On paper, things don’t always tell the whole story,” he says. “Part of the job is understanding whether something is normal-messy or dangerous-messy.”

A temporary dip tied to supply chain disruptions may be manageable. The loss of a major customer may not be. “You have to listen to the business owner and understand what’s driving the numbers,” he says. “If we structure a loan that doesn’t work for their cash flow, it creates problems for everyone.”

Moran, who also serves on the board of the Federal Reserve Bank of Boston, emphasized that uncertainty, from geopolitical conflict to economic shifts, will remain a constant. “We model best- and worst-case scenarios, but we’re not in the business of predicting rates,” she says. “We stay close to all the data and adjust.”

Making Loans in Difficult Economies

Workforce shortages, housing constraints and energy volatility often present the most pressing non-rate concerns for lenders, Bortolotto says. “Workforce constraints are the number one non-rate lending issue on the commercial side,” he says, pointing to an aging population, limited in-migration and persistent skill gaps across industries. Housing is a close second.

“People don’t want to move to a place where they can’t find a house, affordable or otherwise,” he says.

Rising home prices, limited inventory and higher borrowing costs have pushed many first-time buyers out of the traditional market and created a barrier to workforce development.

In response, institutions like Ledyard Bank are developing targeted solutions. The bank is finalizing a loan program for accessory dwelling units and expanding financing options for manufactured homes—what Moran calls “the new first home.”

“They’ve improved tremendously over the past 10 to 20 years,” she says.

Ledyard has also introduced programs for first responders, healthcare workers and nonprofits, combining lending with advisory services to address broader

economic challenges.

Those efforts intersect with the work of the NH Community Loan Fund, a nonprofit lender that operates outside the traditional banking model to serve borrowers often excluded from conventional financing.

“Our mission is to help people get into the financial mainstream and then, when they’re ready, help them move on to local banks,” says Saltzman.

As a community development financial institution, the NH Community Loan Fund provides financing and coaching to low- and moderate-income borrowers, small businesses and housing developers. It has invested hundreds of millions of dollars statewide, supporting affordable housing, resident-owned communities and local enterprises.

“We’re seeing buyers who can afford a mortgage but don’t have savings for closing costs,” Saltzman says. “That’s where we step in.”

Community banks, he adds, support the work of Community Development Financial Institutions (CDFI’s) like the NH Community Loan Fund through low-rate, long-term capital investments while CDFIs complement the work of community banks through co-lending arrangements.

Community Banks Take Long View

Hamilton says mutual and community banks, which are relationship-driven and focused on small businesses and local lending, can take a longer view than larger national banks.

If a business is struggling today but has a credible path forward, community banks are often willing to work with them, he says.

Those relationships are central to how lending functions at the local level. “At a certain point, every business needs to talk to a person who understands their challenges,” Bortolotto says, adding that community banks frequently collaborate on larger loans, sharing risk to support projects that might otherwise be out of reach.

“When something is too big for one bank, we work together,” he says. “You’re competing, but you’re also collaborating.”

Bortolotto explains the most common form of collaboration is loan participation. This happens when a bank gets close to their legal lending limit, which is tied to their capital position. It also occurs when banks want to preserve their ability to lend to that customer again in the future. They can “participate” a portion of the loan to another bank. “Most of the community bankers collaborate well with each other and maintain those relationships,” he says

Banks also collaborate with the Small Business Administration, NH Business Finance Authority and the Community Loan Fund in similar situations, Bortolotto adds.

For Logan, that collaborative, locally rooted model is what is at stake in a rapidly evolving financial landscape. Where individuals and businesses choose to bank, he says, has direct consequences for the strength of local economies.

“There’s a reason we talk about shopping local and people should think about banking local the same way,” Logan says. “If you bank with a local institution that has a presence in your community, those dollars are going to be reinvested back into that community.”

Hamilton, who also owns his small business, Shire’s Naturals, which makes dairy-free cheese and frozen meals, echoes this sentiment.

“When it works well, you’re not just financing a business, you’re supporting growth that carries through the local economy,” he says, adding that in a higher rate environment, aligning the loan structure with how the business actually generates cash becomes even more important.

That reinvestment is not just a philosophy, it is embedded in federal policy through requirements that banks lend within the communities they serve. But it also depends on maintaining a strong base of local deposits.

“Banking local helps ensure that lending continues in your community,” Logan says. “And that’s essential to the long-term health of the state’s economy.”

Bortolotto says one of the best parts of his job is being able to see his bank’s lending support help small businesses grow over time. “It’s fascinating to see the passion business owners have,” Bortolotto says. “You might give someone a $20,000 line of credit early on, and years later they’re running a $20

million company.”