KEY POINTS

-

- The Business Enterprise Tax (BET) is a unique New Hampshire State tax on compensation, interest, and dividends paid by organizations in the state

- BET rate reductions have decreased revenue available for public services since reductions began in 2015

- A currently-proposed BET rate reduction would have very limited impact on the tax liability of all but the largest BET filers, while reducing BET revenue by more than $26 million annually if it had been in place this budget cycle

- Average taxpaying filer savings from the proposed rate reduction would be about $565, based on 2023 data

- Economic benefits associated with State business tax rate reductions are not clear, and research from other states reach mixed or limited conclusions about benefits of corporate tax reductions.

Past reductions in the New Hampshire Business Enterprise Tax (BET) have lowered the amount of revenue available for public services. Those rate reductions have not provided clear economic benefits, and a newly-proposed rate reduction does not appear likely to spur significant changes in private-sector economic activity.[1]

The proposed BET rate reduction, which would lower the BET rate from 0.55 percent to 0.5 percent, would generate very small tax savings for most companies paying the BET. Only a few of the largest companies would see their liabilities reduced enough to consider hiring another worker. However, if the rate reduction had been in full effect for the current State Budget, BET revenue would likely have been lower by more than $26 million per year in each year of the budget biennium.

That total is equivalent to more than half the road and bridge aid sent by the State to municipalities through the State Budget in State Fiscal Year (SFY) 2025. This annual amount is also more than half the SFY 2025 budget of the New Hampshire Veterans Home, the Division of State Police, or the Bureau of Children’s Behavioral Health.[2]

What is the Business Enterprise Tax?

Unique among state tax revenue sources across the United States, the New Hampshire Business Enterprise Tax (BET) is fundamentally a tax on compensation paid by businesses. According to the statute establishing the BET, that tax base is the “sum of all compensation paid or accrued, interest paid or accrued, and dividends paid by the business enterprise,” with certain adjustments to avoid double taxation and to exclude out-of-state activity.[3] “Compensation” is defined as “all wages, salaries, fees, bonuses, commissions, or other payments paid directly or accrued by the business enterprise in the taxable period on behalf of or for the benefit of employees, officers, or directors of the business enterprise,” including taxable self-employment income.[4] The BET was created in 1993 following a lawsuit against the State of New Hampshire from a large company that alleged the State taxed companies unfairly through the New Hampshire Business Profits Tax (BPT); many smaller for-profit entities did not face significant BPT liability, particularly those that would primarily increase compensation in response to higher earnings, so the BET was created to tax smaller businesses for which compensation was a focus of revenue use, rather than profits.[5]

Not all businesses paying compensation in the State owe BET. The BET has two components to its filing threshold: the business must have both gross receipts and a BET base under a certain value that is adjusted for inflation every year; businesses with values above either threshold must file, but they do not necessarily have to pay. The filing thresholds for Tax Year 2025 are $298,000 for both gross receipts and the tax base.[6]

Many business entities registered with the State likely have smaller operations that do not meet the filing threshold. The New Hampshire Secretary of State’s Office had approximately 205,000 businesses registered and in “Good Standing” or “Active Status” as of October 2024, while there were 77,526 BET filers in Tax Year 2022 and 73,980 filers in Tax Year 2023’s available data to date. Even among filers, however, 44.3 percent did not owe any BET in Tax Year 2022, and 45.1 percent did not owe any BET in Tax Year 2023.[7] Some entities are not required to file or pay, however; for example, the Secretary of State’s Office indicated that about 76,817 domestic Limited Liability Companies provided annual reports in the five years leading up to 2024, and these entities would likely not have to file BET based on their structures.[8]

How could the proposed rate reductions lower the amount of BET businesses pay?

The most recent proposal to reduce the BET rate would lower it from 0.55 percent to 0.50 percent. If that 0.50 percent rate had been in full effect during the current State Budget biennium, BET revenues would likely have decreased by about $54 million during those two years, based on State Budget revenue projections.

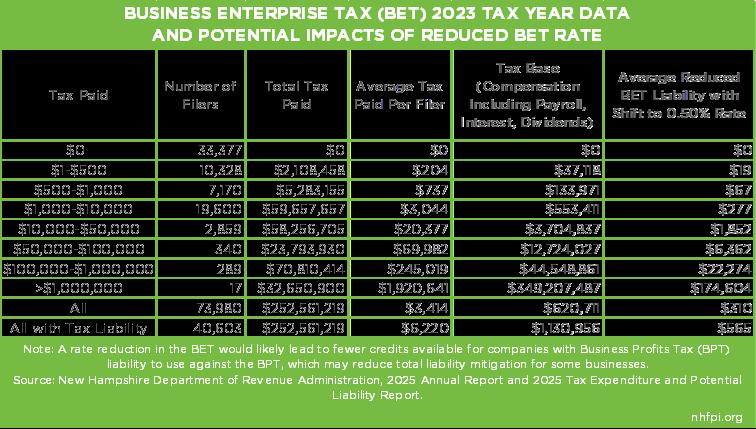

For individual businesses, the effects are unlikely to substantially change economic and investment behavior, particularly at the scale that would be required to spur significantly more hiring in the state. Among the 40,603 BET filers who had a tax liability in Tax Year 2023, the average BET tax base, likely primarily representing payroll expenses, was about $1.1 million. The amount of reduced tax liability from the proposed lower BET rate would have been $565.48 for the average paying filer that year. The largest 306 tax filers, which had an average tax base of $61.5 million each, would see their BET liability reduced by $30,737.17. The remaining filers with liability, with an average tax base of $672,732, would experience an average tax reduction of $336.37. Only the largest few entities filing would see savings sufficient to hire more than a few people.

Additionally, savings could be further limited by the loss of BET credit against the BPT. Businesses that owe BPT may have fewer BET credits to offset their BPT liability. If the rate of use of BET credit matches the aggregate amount of BET credit used, then only a few hundred of the largest filers will see tax reductions greater than $2,000, and very few would have a tax reduction sufficient to hire any new employees. The rate of use of the BPT credit is not certain, however, particularly across filter liability sizes.

Who pays the Business Enterprise Tax?

A broad array of organizations that pay their employees compensation are required to pay BET, but there are significant exceptions. For example, organizations that are nonprofit 501(c)(3) entities under federal tax law are not required to pay BET.[9]

There are credits that businesses can report to reduce their BET liability, including for certain research and development credits, certain contributions to education scholarships or funding for the State’s Division of the Arts, for job creation in Coos County, or for expenses incurred by a business to offer paid family and medical leave to their employees. The amount of BET paid itself can be used as a credit against the BPT, which collects substantially more money each year and offsets the BPT liability for smaller, profitable businesses paying BET for compensation. A business has to be profitable, under the State’s required calculations, to owe BPT, but does not need to earn a profit to owe BET.[10] In State Fiscal Year (SFY) 2025, approximately $187,468,000 of BET credits, or the equivalent of 74 percent of the BET liability on returns filed that year, were used to offset BPT liability. However, this comparison does not indicate that these credits were directly used, as they do not need to be used in the year.[11] The percentage also varies over time; for Tax Year 2018, the State calculated a credit use rate of 61 percent using similar datasets.[12]

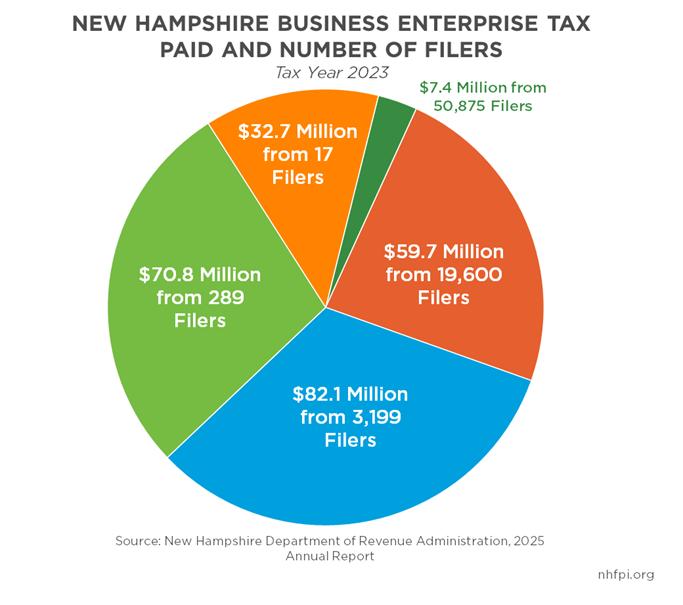

Of the 73,890 BET filers for Tax Year 2023, according to the latest available data, 50,875 owed less than $1,000 in BET, suggesting a tax base of a maximum of about $182,000. Of that group, 33,377 (65.6 percent) filed but owed no BET, potentially due to using a tax credit. On the other end of the scale, 17 filers that owed $1 million or more each individually paid $32.7 million in total, or 12.9 percent of the total BET revenue collected in Tax Year 2023. The 289 filers paying more than $100,000 but less than $1 million each individually paid an additional $70.8 million, or 28.0 percent of the total BET revenue collected for Tax Year 2023, according to the latest available data.[13]

The type of business tax filer also provides insights into the organizational structure of businesses paying BET. Partnerships, proprietorships (including self-employed sole proprietors), and fiduciaries together comprised 53.5 percent of all filers in Tax Year 2023, but only 19.3 percent of the revenue collected. Corporations accounted for 39.0 percent of filers and 28.3 percent of total revenue. About 52.4 percent of all BET revenue was paid by “Water’s Edge” filers, which are multi-part businesses that report as one combined filer, and may (but do not necessarily) have component businesses operating primarily outside of the United States; while paying more than half of BET revenue collected, these Water’s Edge filers included 5,493 entities, comprising 7.4 percent of filers that year.[14]

Businesses operating in multiple states, including businesses with potentially taxable activity in other states, pay BET based on an apportionment formula used to determine the amount of taxable business activity attributable to New Hampshire. The basic construction of the formula requires a multi-state business to identify total amount paid to employees for services within New Hampshire as a percentage of all compensation for all employes of the company located everywhere. The interest component of the apportionment formula is based on the percentage of real and tangible property owned within the state relative to all property, and the dividend part of the tax base is apportioned using compensation, interest, and sales within the state as a fraction of total sales. These percentages, representing activity in New Hampshire as a portion of all the business’s activity, are applied to the tax base to help determine the amount owed to New Hampshire, rather than attributable to economic activity elsewhere. The Water’s Edge election that combined filers paying BPT can use to exclude profits attributed to international components of their businesses does not apply to the BET calculations.[15]

The average BET paid by businesses filing in Tax Year 2023 was $3,414 for all filers. Including only businesses paying BET, rather than filing for BET but not owing any taxes, the average BET paid was $6,220. Excluding the 306 filers with more than about $18.2 million in BET base, the average BET paid by those 40,297 filers with any liability was $3,700.[16]

What has happened to the BET rate over time?

The BET rate is relatively low compared to most rates of other taxes because it has a comparatively broad tax base. The estimated tax base, primarily driven by compensation paid by businesses, in Tax Year 2023 was $45.9 billion. For context, New Hampshire’s Gross State Product, a measure of the size of the state’s economy, was $114.4 billion in 2023, although not all BET taxable activity is necessarily reflected directly within Gross State Product.[17]

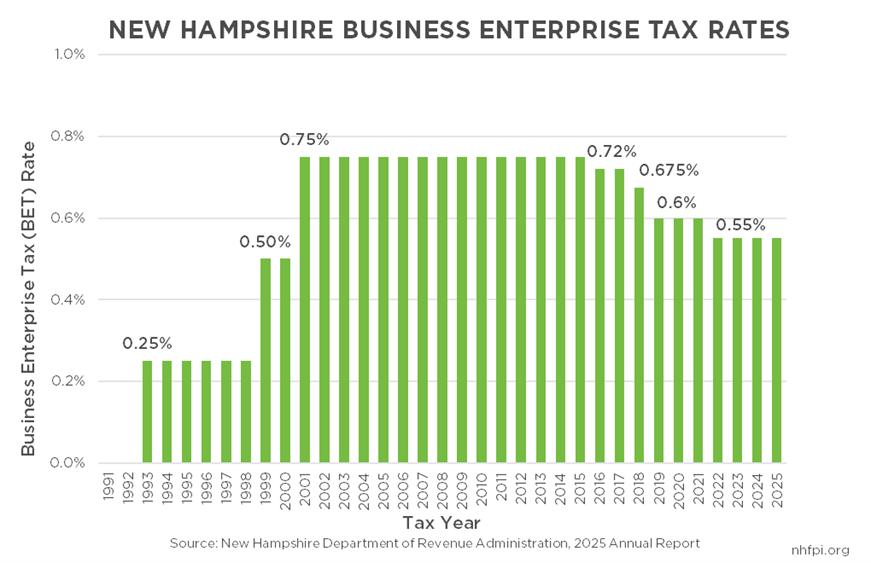

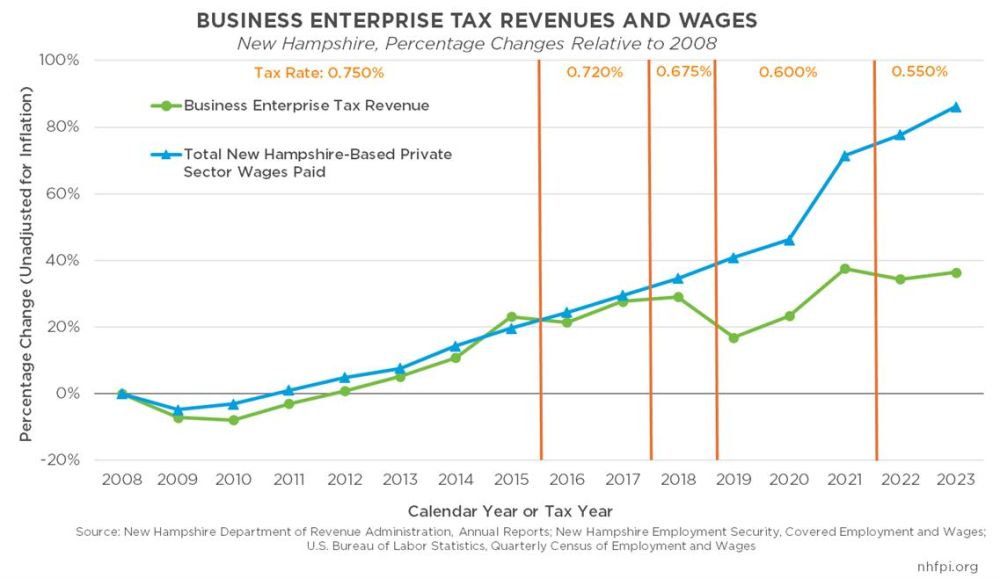

As a result, the BET can raise a significant amount of resources for State services without a high rate. The current BET rate is 0.55 percent. The BET rate started at 0.25 percent, and the highest rate the BET has been in its history was the 0.75 percent rate, three quarters of one percentage point, from 2001 to 2015.

Since 2015, legislators have approved four rate reductions to the BET. The longstanding rate of 0.75 percent, which was increased to that level to help establish and fund the State’s Education Trust Fund, was lowered to 0.72 percent for Tax Years 2016 and 2017; the rate was lowered again to 0.675 percent in Tax Year 2018. There was a further reduction in Tax Year 2019 to 0.6 percent, and the most recent reduction was to 0.55 percent in Tax Year 2022. BPT rates were lowered on nearly the same schedule.[18] The currently proposed BET reduction would lower the rate to 0.50 percent.[19]

What have the revenue effects of the rate reductions been in recent years?

The BET rate reductions have lowered revenue for public services coming into the State relative to the amount of revenue that would have been collected under 2015 rates. From 2008 through 2015, there was a strong correlation between total wages and salaries paid by private sector businesses to New Hampshire-based employees and reported through the State’s unemployment insurance system and BET revenues. As compensation is a key component of the BET base, these changes logically drive BET revenue when all other factors, such as the tax rate, remain the same.[20]

After each rate reduction during the last decade, BET revenues have broken from the trend of following total private-sector wages paid in the state. The BET growth trend returns to largely matching growth in private-sector wages in the years after each rate reduction, but at a lower level resulting from that initial decline. These data show that growth in the tax base has not offset the revenue forgone by the rate reductions.[21]

If the BET rate had not been lowered since 2015 and BET revenues had maintained the same relationship with private sector wages in New Hampshire over time, the BET would have likely collected between $376 million and $553 million more in revenue from Tax Years 2016 through 2024; this figure does not include any contemporaneous changes in BPT revenues. This range reflects the potential economic feedback associated with potential higher growth rates in response to lower tax rates. However, the evidence for such economic feedback existing is limited and inconclusive, as outlined in NHFPI’s August 2023 analysis of both BET and BPT rate reductions titled State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services. This analysis also describes the methodology used to calculate the BET revenue loss figures, updated with the most recent available data, presented in this analysis.[22]

Public services are funded based on State fiscal years, rather than tax years, in each State Budget cycle. The impacts of the rate reductions on the current State Budget can be estimated using the revenue projections for business taxes established by policymakers for the current SFYs 2026-2027 State Budget, the recent historical relative size of BET and BPT revenues as a percentage of total business tax revenues, and the estimates available for the percentage of BET reductions offset by an increase in BPT revenue resulting from fewer available BET credit dollars against BPT liabilities. Revenue forgone by the BET rate reductions alone would total approximately $215 million during the State Budget cycle, assuming no economic feedback.

If the proposed 0.50 percent rate reduction had been fully implemented ahead of the SFYs 2026-2027 biennium, revenue during the biennium would have likely been about $269 million, or $131 million in SFY 2026 alone, relative to if the BET rate had remained at 2015’s 0.75 percent.

In SFY 2025, the equivalent of 74 percent of BET liability was used as a credit against the BPT. Some of those credits may have been carried forward from prior years, and the credits can only be used by businesses with a BPT liability. If 74 percent of BET credits would have been used against the BPT, the total BPT and BET revenues would have been $57 million lower if the BET rate alone had remained at 2015 levels during the State Budget biennium.[23] An analysis conducted by the New Hampshire Department of Revenue Administration for Tax Year 2018 found the equivalent of a feedback of 61 percent in BET credits used against the BPT; that level of feedback would result in forgone revenue over the biennium of $84 million.[24]

If the proposed rate reduction to 0.50 percent for the BET had been in full effect and the BET credits lost had been used at the 74 percent rate, then the total revenue loss for the SFYs 2026-2027 biennium would have been $14 million. The more conservative 61 percent rate would suggest a loss of $21 million. However, the New Hampshire Department of Revenue Administration often does not include this BPT revenue boost from a BET rate reduction in its revenue projections; the feedback varies annually and is subject to significant uncertainty.[25]

Didn’t revenue from business taxes increase between 2015 and 2024?

Combined revenue from the BPT and the BET increased $664 million, or 118 percent, between SFYs 2015 and 2024.[26] However, revenues from this period were still diminished by business tax rate reductions. Five key factors help explain the increases while rates declined:

- While revenues increased, they were lower than they would have been without the rate reductions. Revenue increased more slowly than it would have otherwise over this period.

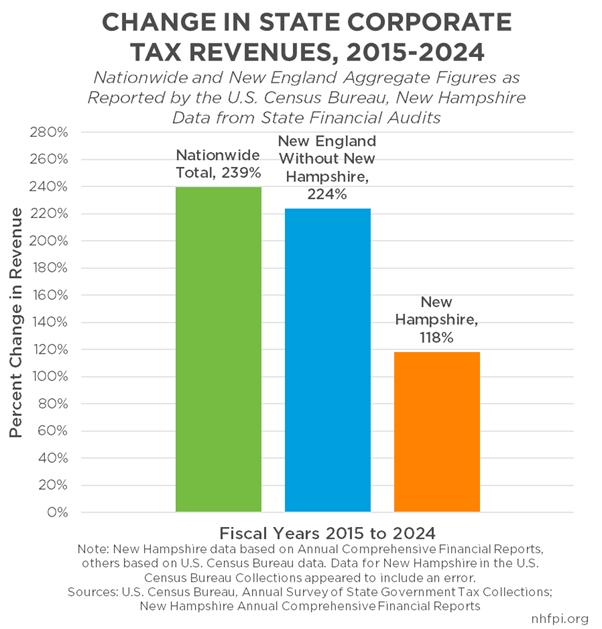

- State corporate tax revenues increased nationwide during this period, and increased faster than New Hampshire’s business tax revenues in aggregate. Between fiscal years 2015 and 2024, corporate tax revenues rose 239 percent nationally, and increased 224 percent in the other five New England states combined. Every other state in New England saw a faster increase in state corporate tax revenues than New Hampshire during this period.[27]

- The BPT, which is driven in part by changes in national corporate profits, accounts for about three-quarters of the revenue collected by the business taxes combined. Increases in BPT revenue, including those caused by factors beyond New Hampshire policy decisions, can overwhelm and mask changes in BET receipts.[28]

- Examining changes by State fiscal year do not show the impacts of the tax rate reductions clearly. Businesses submit quarterly estimate payments throughout the year, but base those estimates on the tax rate in the tax year, rather than the State fiscal year. For example, BET returns filed in April 2016 reflected the 0.75 percent tax rate in Tax Year 2015, but the quarterly estimate payment submitted by the same business in April reflected the lower 0.72 percent tax rate that was to take effect for Tax Year 2016; both these payments, at different tax rates, occurred during SFY 2016. As a result, payments based on tax years can be spread across several State fiscal years, and changes in revenues in State fiscal years are difficult to clearly attribute to changes in tax policy that are made on a tax-year basis.

- Using tax year data, BET revenues were lower following the rate reductions, even without adjusting for inflation. Revenues were lower in Tax Year 2016 than in Tax Year 2015, following a rate reduction for 2016. BET revenue was also lower in Tax Year 2019, following another rate reduction, than they were in any year since Tax Year 2014. BET revenue was also lower in Tax Year 2022 relative to Tax Year 2021 following a rate reduction.[29]

Did the past rate reductions help the economy?

While revenue clearly did not increase as a result of BET rate reductions, conclusions about the economic impact of BET rate reductions are more difficult to determine.

There is no strong statistical relationship between BET rates and job growth over the last four decades. An analysis of annual job growth in New Hampshire from 1983 to 2024, including the decade before the BET’s implementation with a 0.0 percent tax rate, did not reveal a relationship indicating BET rates impact job growth.[30] While there are many ways to measure the health of the economy, the BET’s primary function as a tax on compensation suggests that employment growth would be more likely than other measures to be impacted by BET changes.

Analyses of corporate tax rate reductions, including at the state level, do not indicate reducing state corporate tax rates is likely to increase revenue, or have a dramatic effect on economic activity overall. Research is mixed as to whether changes in state tax policies have significant effects on state and local economies. In a December 2015 literature review published in National Tax Journal, authors found “[m]ajor recent studies reach almost every conceivable finding: tax cuts raise, reduce, do not affect, or have no clear effect on growth.” Relative to state corporate taxes, the authors of that analysis identified several studies that show no statistically significant negative effects of corporate tax rates on economic growth, while some research suggests that higher property taxes have negative impacts.[31]

Referring to the BPT, New Hampshire’s Commission to Study Business Taxes, which released its final report in 2014, wrote “[t]he Commission had no basis for concluding that any effect of attracting new businesses or business expansion as a result of a rate reduction would generate additional tax revenue sufficient to compensate for the revenue loss that would result from the rate reduction.”[32]

Concluding Discussions

Past BET rate reductions have lowered revenue available for public services. These rate reductions, as well as their BPT counterparts, have not brought clear economic benefits to the state. The dollar amounts of reduced tax liability with these rate reductions on a per-business basis, particularly the proposed rate reduction of five-one-hundredths of a percentage point, are typically small relative to overall operations. A tax rate reduction is unlikely to generate more economic activity.

Conversely, the revenue forgone resulting from a BET rate reduction at the State level could be significant. The interaction between the BPT and the BET has the potential to offset some of the revenue lost in a BET rate reduction. However, such interactions are less certain than the decline in revenue overall. Policymakers just used $67.3 million from the State’s Rainy Day Fund to help cover costs that outpaced revenues and limited key services in the new State Budget; revenue reductions associated with a BET rate change would likely lead to further curtailment of public services for Granite Staters.

End Notes

[1] For more information and analysis of the economic impacts of past business tax rate reductions in New Hampshire and corporate tax rate changes in other places, see NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services and NHFPI’s April 2025 Issue Brief Business Tax Rate Reductions Led to Between $795 Million and $1.17 Billion in Forgone Revenue for Public Services Since 2015. For the newly-proposed legislation, see House Bill 155 of the 2025/2026 Legislative Sessions.

[2] See the Office of Legislative Budget Assistant’s State Aid to Cities, Towns, and School Districts, Fiscal Year Ending June 30, 2025. See also the Governor’s Executive Budget Summary, State of New Hampshire Budget for Fiscal Years Ending June 30, 2026-2027.

[3] See RSA 77-E:1, IX, RSA 77-E:3, and RSA 77-E:4.

[4] See RSA 77-E:1, V.

[5] For more information, see the State of New Hampshire’s Commission to Study Business Taxes, Final Report, October 30, 2014.

[6] See the New Hampshire Department of Revenue Administration’s TIR 2024-004 from December 17, 2024.

[7] See the New Hampshire Department of Revenue Administration’s 2025 Annual Report, pages 44-48.

[8] For more information, see the Secretary of State’s Office Comprehensive Business Data dashboard.

[9] See RSA 77-E:1, III.

[10] See RSA 77-E and the New Hampshire Department of Revenue Administration’s 2025 Tax Expenditure and Potential Liability Report.

[11] For more information, see the New Hampshire Department of Revenue Administration’s 2025 Tax Expenditure and Potential Liability Report.

[12] See the New Hampshire Department of Revenue Administration, Governor’s Office Request to Model State Tax Change Proposals, February 22, 2021.

[13] Tax Year 2023 data represent recorded and aggregated tax returns as of July 21, 2025. For the full breakdown, see the New Hampshire Department of Revenue Administration’s 2025 Annual Report, page 47.

[14] For the data for Tax Year 2023, see the New Hampshire Department of Revenue Administration’s 2025 Annual Report, page 47. For a description of “Water’s Edge” filers, see NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services.

[15] For more details, see RSA 77-E and the New Hampshire Department of Revenue Administration’s tax forms. Information for this paragraph was also provided directly by the Department of Revenue Administration.

[16] Calculations conducted using the New Hampshire Department of Revenue Administration’s 2025 Annual Report, page 47.

[17] Estimate last updated by the U.S. Bureau of Economic Analysis on September 26, 2025.

[18] For more information on past rate reductions, including for the Business Profits Tax, see NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services and NHFPI’s April 2025 Issue Brief Business Tax Rate Reductions Led to Between $795 Million and $1.17 Billion in Forgone Revenue for Public Services Since 2015.

[19] See House Bill 155 of the 2025/2026 Legislative Sessions.

[20] For more information and statistical testing of this relationship, see NHFPI’s August 2023 Issue Brief Business Tax Rate Reductions Led to Between $795 Million and $1.17 Billion in Forgone Revenue for Public Services Since 2015.

[21] The data reporting private-sector wages paid to employees based in the state are reported by the U.S. Bureau of Labor Statistics and is related to the data reported by New Hampshire Employment Security in the Covered Employment and Wages dataset.

[22] For more information on past New Hampshire tax rate reductions and the methodology used to calculate revenue forgone by the BET rate reductions, see NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services and NHFPI’s April 2025 Issue Brief Business Tax Rate Reductions Led to Between $795 Million and $1.17 Billion in Forgone Revenue for Public Services Since 2015.

[23] This analysis applies the average of the last five years of the historical splits between BPT and BET revenues, calculated from the New Hampshire Department of Revenue Administration’s annual reports, for Tax Years 2019 through 2023. It applies this percentage of total business tax revenue attributable to the BET, which 25.7 percent, to the projected business tax revenues incorporated into the SFYs 2026-2027 State Budget. After isolating the BET component, it then uses the current 0.55 percent tax rate to estimate the BET base. Using those tax bases for SFYs 2026 and 2027, the analysis then applies the rate of 0.75 percent to the BET base to calculate the amount of revenue that would have been collected at that higher rate. To adjust for potential BPT liability reductions because of the increased BET credits that would have been available, the analysis uses the reported BET credit used in SFY 2025 as a percentage of all BET liability reported on tax returns that year from New Hampshire Department of Revenue Administration’s 2025 Tax Expenditure and Potential Liability Report, as well as the 61 percent calculated by the Department in 2021 and based on Tax Year 2018 in the document Governor’s Office Request to Model State Tax Change Proposals, February 22, 2021.

[24] See the New Hampshire Department of Revenue Administration, Governor’s Office Request to Model State Tax Change Proposals, February 22, 2021.

[25] The fiscal note for House Bill 155 of the 2025/2026 Legislative Sessions does not include BPT revenue recoupment, for example.

[26] These calculations are based on the State’s Annual Comprehensive Financial Reports.

[27] This analysis uses the U.S. Census Bureau’s Annual Survey of State Government Tax Collections for all non-New Hampshire states and the State’s Annual Comprehensive Financial Report data for New Hampshire, due to an apparent error in the U.S. Census Bureau’s data for New Hampshire’s fiscal year 2015 collections.

[28] See NHFPI’s May 2019 Issue Brief Funding the State Budget: Recent Trends in Business Taxes and Other Revenue Sources, NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services, and NHFPI’s April 2025 Issue Brief Business Tax Rate Reductions Led to Between $795 Million and $1.17 Billion in Forgone Revenue for Public Services Since 2015.

[29] Tax year data are available from the New Hampshire Department of Revenue Administration’s Annual Reports.

[30] This regression, which explored the relationship between the BET rate and job growth, yielded an R2 value of 0.09, suggesting very little explanatory power for variations in job growth from the BET rate. The regression’s p-value for the equation’s coefficient was 0.06, which was not statistically significant at the 95 percent confidence level. While it is significant at the 90 percent confidence level, the explanatory power of BET changes would be very limited even if there were a relationship, based on these data.

[31] See The Relationship Between Taxes and Growth at the State Level: New Evidence as published in December 2015 in the National Tax Journal. See also the reviews, research, and references in NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services and NHFPI’s April 2025 Issue Brief Business Tax Rate Reductions Led to Between $795 Million and $1.17 Billion in Forgone Revenue for Public Services Since 2015.

[32] This sentence references the State of New Hampshire, Commission to Study Business Taxes, Final Report, October 30, 2014.

The New Hampshire Fiscal Policy Institute is sharing these articles with the partners in The Granite State News Collaborative. NHFPI is an independent nonprofit organization that explores, develops and promotes public policies that foster economic opportunity and prosperity for all New Hampshire residents. For more information visit nhfpi.org. These articles are being shared by partners in The Granite State News Collaborative. For more information visit collaborativenh.org.