KEY POINTS

-

- The 2025 federal reconciliation law made changes to the Child Tax Credit, the Child and Dependent Care Tax Credit, and two other early care and education-related credits.

- The Child and Dependent Care Tax Credit expansion allows more child care expenses to be offset by the tax credit, but remains nonrefundable, leaving families with lower incomes without expanded access to benefits.

- The Child Tax Credit expansion increases benefit maximums for middle and upper-middle income households, but leaves supports for households with lower incomes largely unchanged.

- Two other tax policy changes decrease costs for employers seeking to provide benefits to employees.

Several key federal tax policy changes are impacting the refunds Granite Staters are receiving this tax season, particularly families with children. These tax changes may help some households better afford the costs of caring for children, including additional assistance for early care and education

Enacted on July 4, 2025, the new federal reconciliation law (H.R. 1 or the One Big Beautiful Bill Act) introduced a series of changes to tax policy and federal programs. Many of these new and modified provisions are already beginning to shape the lives of people across the country, including Granite Staters, through both direct changes to household finances and indirect shifts in federal benefits and economic incentives.[1] As these modifications continue to take effect, they will influence how families, workers, policymakers, and businesses make financial decisions.

Included in the 2025 reconciliation law were changes to provisions related to child tax policy, notably the Child Tax Credit (CTC) and Child and Dependent Care Tax Credit (CDCTC), both of which are designed to offset costs associated with raising a child, including child care expenses. Both the CTC and CDCTC saw revisions in the 2025 reconciliation law that will primarily serve to expand, but in some cases limit, their capacity for providing financial relief for families, particularly those facing the greatest economic insecurity.[2]

Together, these changes come at a time when the cost of raising children remains high in New Hampshire. As the costs associated with raising a child continue to rise, these tax policy changes will have a direct impact on child care affordability and access to quality care for Granite State families and children. In recent years, New Hampshire families have faced a growing affordability crisis, particularly as it relates to expenses associated with raising children.[3] While costs of these expenses such as food and diapers have risen, child care costs remain one of the leading financial burdens for Granite State families.[4] Center-based child care for an infant and a 4-year-old in New Hampshire averages $30,000 per year. That amounts to about 24% of the median family income for a married couple with two or more children under 5 and 58% of income for a single or unmarried mother.[5]

Tax policies designed to support households with children, such as the CTC and CDCTC, have considerable potential to mitigate the budgetary strains New Hampshire families endure to afford child care and other related costs, but are less effective for families with low and moderate incomes, who may not earn enough to fully benefit from the credits.[6]

Child and Dependent Care Tax Credit Changes

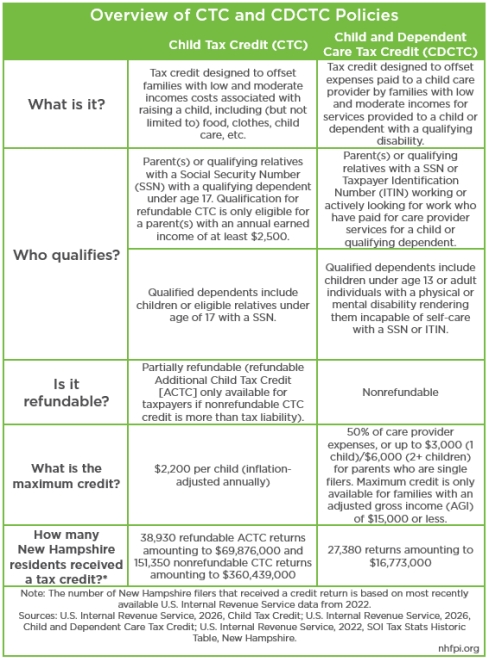

First enacted in 1976, the Child and Dependent Care Tax Credit (CDCTC) is a federal tax credit that helps working families offset a portion of the costs they pay for child care services so they can work or look for work. Eligible families can claim a percentage of qualifying expenses on their annual federal tax return for the care of a child under age 13 or a dependent of any age who is physically or mentally incapable of self care. Qualifying expenses include a broad range of care settings, such as licensed child care centers, family child care homes, afterschool programs, summer day camps, as well as some licensed exempt providers, such as faith-based providers and in-home caregivers, as long as the care enables parents to maintain employment.[7]

The CDCTC has been changed considerably by the U.S. Congress over the last ten years. The long-standing structure was altered by the 2017 Tax Cuts and Jobs Act (TJCA); this legislation retained the credit as non-refundable and set the maximum credit to 35% of permissible costs. Without full refundability, the CDCTC was most useful to families that had enough tax liability that the credit could be used to offset the amount paid, meaning that families with moderate incomes benefited, but the lowest income families could not receive the full credit amount because they lacked the initial tax liability to use the credit against.[8]

In 2021, the American Rescue Plan Act (ARPA) temporarily expanded the CDCTC by increasing the maximum value to 50%, raising the share of eligible expenses that could be counted and extending the income eligibility threshold. Critically for families with the lowest incomes, particular those incomes under $15,000 per year, ARPA also made the credit fully refundable for one year, which allowed many families with low and moderate incomes who were previously ineligible to have access to the full credit. After this temporary expansion ended, the CDCTC returned to its earlier nonrefundable structure with a lower maximum benefit.[9]

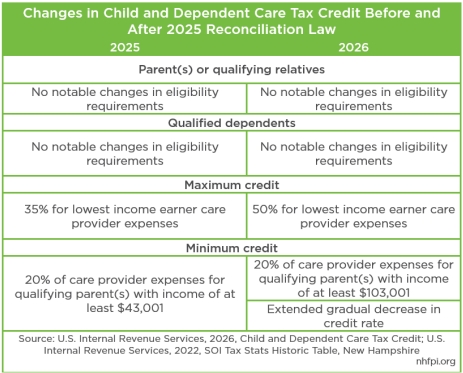

Following permanent changes made in the 2025 reconciliation law, the 2026 credit remains aligned with the more traditional nonrefundable framework that existed in 2025, reflecting the temporary nature of the ARPA design and offering a more limited benefit compared to the temporary 2021 expansion that had broadened access for many families. The maximum credit rate expanded from 35% to 50% (or up to $3,000 for one child and $6,000 for two or more children) for the lowest income families, however, the credit rate remains nonrefundable, limiting the potential financial impact that the credit can have for these families.[10]

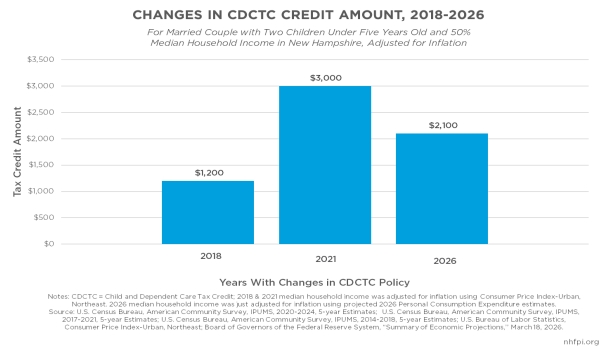

The CDCTC expansion in place following the 2025 reconciliation law will provide some additional financial relief for Granite State families starting when Tax Year 2026 refunds are being provided, although less aid than many experienced under the ARPA expansion.[11] A married couple in New Hampshire with two children under five that made $65,441 of taxable annual income, equating to 50% of the median annual family income in 2026 would be eligible to receive up to $2,100 (35%) nonrefundable credit for their child care provider expenses under the 2025 reconciliation law expansion.[12] Prior to the expansion, that same family would have only been eligible for a credit equivalent to $1,200 (20%) of permissible expenses, though still considerably lower than the fully-refundable $3,000 (50%) under the temporary ARPA expansion.

In New Hampshire, there are approximately 146,975 married-couple parents and 40,339 unmarried parents with at least one child under the age of 13 years old that could be eligible for at least partial credit through the CDCTC.[13] Of those families, 86,604 have at least one child under 5 years of age.[14] However, based on most recent available tax return data, the CDCTC has historically been underutilized by Granite State families. The largest amount of CDCTC credit accessed was for Tax Year 2021 during the temporary ARPA expansion, which saw an increase from $13.1 million in 2020 to $51.3 million in total credit dollars provided to New Hampshire taxpayers, and later returned back to $16.8 million in 2022. These additional dollars for New Hampshire families, particularly those with low and moderate incomes, likely provided significant relief in offsetting expenses for child care services.[15]

Furthermore, the CDCTC’s credit rates can affect the financial well-being of New Hampshire households differently across racial and ethnic groups given its varying credit rate structure. Among qualifying children, the share within each racial and ethnic group with annual family incomes below $15,000 and eligible for the full 50% credit is 5.1% for children of Hispanic origin, compared to 1.9% for Black or African American children and 1.8% for white children. This indicates that children of Hispanic origin are about 2.8 times more likely than white children to have parents with incomes below $15,000, despite comprising only 8% of all qualifying children under 13 years of age. However, since the CDCTC is nonrefundable, these families with less than a $15,000 annual income would likely owe little or no income tax and therefore cannot claim the credit, meaning they receive little or no benefit even if they do qualify for the maximum 50% rate.[16] The Tax Policy Center estimated that the maximum credit amount that a family would likely receive would be about $2,100.[17]

Child Tax Credit Changes

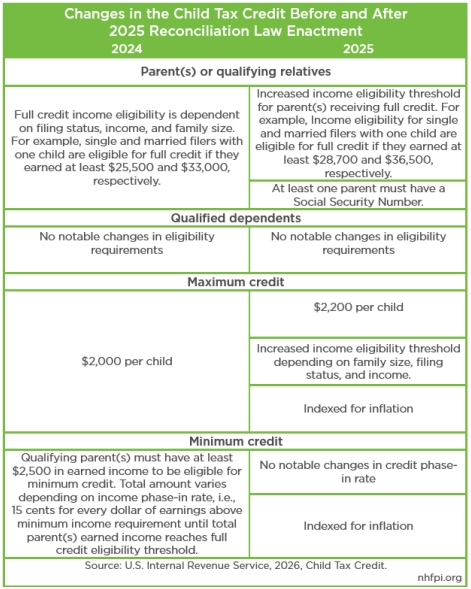

Enacted in 1997, the CTC is a federal tax credit that may be claimed by eligible filers with qualifying children to offset expenses associated with raising children, including, but not limited to, food, clothing, and child care services.[18] Eligible filers must have a dependent under the age of 17 years old who has lived in the same household as the filer for more than half of the tax year. The CTC is partially refundable, with a portion of the credit, referred to as the Additional Child Tax Credit (ACTC), being the only refundable component of the credit. In order to be eligible for the ACTC, filers must have at least $2,500 in annual income. The partial refundability and absence of prescriptive qualifying expenses allow for the CTC to be a key source of financial relief for families with low and moderate incomes.[19]

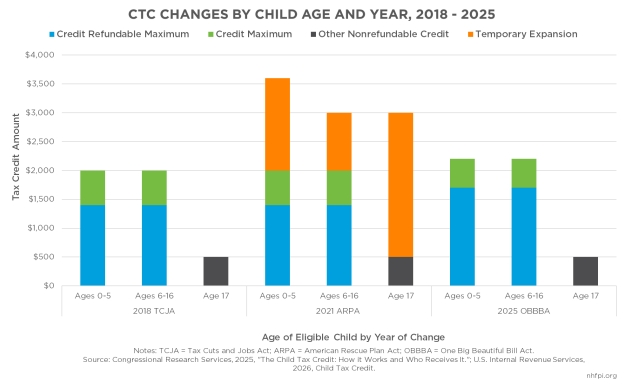

Similar to the CDCTC, the CTC has also seen significant revisions in recent years through successive changes to federal law. The 2017 TCJA set the credit at a maximum of $2,000 per child with only partial refundability. In 2021, ARPA temporarily expanded the credit by increasing it to $3,600 for children under six and $3,000 for children ages six through seventeen, while also making the credit fully refundable. The expanded credit was also delivered in part through monthly installments during the second half of 2021, rather than a delayed delivery in a larger tax refund.[20]

While temporary, this ARPA expansion provided significant economic relief for families with low and moderate incomes, particularly those who had insufficient income to take advantage of the nonrefundable components of the credit under prior law. The ARPA expansion to the CTC, as well as additional one-time Economic Impact Payments that were commonly referred to as “stimulus checks,” were responsible for lifting an estimated 2.9 million children out of after-tax poverty nationally, about 8,000 of whom were Granite Staters.[21]

After this temporary expansion ended, the credit returned to the TCJA structure with a $2,000 maximum and limited refundability, and many of the children who had received temporary economic reprieve slipped back into poverty. Under the most recent 2025 reconciliation law, the credit was expanded modestly to $2,200 starting for Tax Year 2025, with future inflation adjustments incorporated into the law, while retaining partial refundability; it also implemented a requirement that both parent and dependent have a valid Social Security Number. As these changes took effect for Tax Year 2025, they are impacting the refunds received by families during this Spring 2026 tax season.[22]

Unlike the CDCTC, the CTC phases in gradually based on income and family size before a family can be eligible for the full credit. As a result of the expanded CTC, the threshold to be eligible for the full refundable portion of the credit was also raised. The credit phases in at a rate of 15 cents for each additional dollar earned above that threshold, until a family’s income reaches the $1,700 refundable cap. The additional $500 nonrefundable amount can be used as a tax deduction if the filer’s tax liability is above $500. This phase-in rate process excludes families with the lowest incomes from being eligible for the full credit. This means that families are only eligible for the full $2,200 per child credit if they make between an estimated $30,000 and $50,000, depending on tax filing status and family size, or a larger amount. Consequently, the most economically disadvantaged children, including many children of color, children in rural areas, and children in single-parent families, will be among the most impacted by the continued ineligibility to receive full credit.[23]

Additionally, in response to the new requirement that both parents and dependents have a valid Social Security Number rather than only the dependent requiring one under prior law, some families and previously-eligible children will be excluded from eligibility entirely.[24] This change has implications for certain children’s access to high-quality child care services, as the costs for enrollment continue to climb.[25]

Some New Hampshire families eligible to receive the full CTC may see an increase in credit following the 2025 reconciliation law. However, since the phase-in rate was left unchanged, the share of families ineligible to receive the full credit as a result of not meeting the increased annual income threshold could increase.[26]

For example, a New Hampshire family of five with three children under the age of 17 with an annual income of $39,000 and a tax liability of at least $1,500 would have been eligible for the full $6,000 ($2,000 per child) credit prior to the 2025 reconciliation law; under the new changes, that same family would now need an annual family income of $46,500 to be eligible for full credit.[27] Assuming eligible tax liability amount and tax filing status, an estimated 178 married-couple and 2,124 single-parent Granite State households with annual incomes between $25,000-$38,000, who also have one to four children under 17 years of age, will only be eligible for the previous full credit of $2,000 per child and not the expanded $2,200 per child amount.[28] Excluding these families from the increased income eligibility to receive the expanded CTC results in an estimated $984,000 in financial relief for these families with low incomes not being provided, relative to if those families could receive the full credit, at a time when family costs for raising children have been rising significantly.[29] Families filing jointly with a household income up to $400,000 are eligible for the full CTC expansion credit, whereas families that were previously ineligible for the full CTC who have not seen a significant change in their annual income, will not receive an increase in their credit amount. Based on most recent available tax filing records for New Hampshire, 21% of CTC returns were issued to filers with an annual income between $50,000 and $400,000, most of whom would have been eligible for the full credit amount, including the expanded credit amount.[30]

While the CTC expansion enacted in the 2025 reconciliation law provides additional potential refundable tax credits for families, raising the threshold for meeting full credit eligibility without adjusting the phase-in rate will leave many Granite Staters facing the greatest economic insecurity only eligible to receive partial credit.

Together, these changes highlight both the potential and the limits of federal tax policy in addressing child care affordability for Granite State families.

Additional Child Care Tax Policy Changes

In addition to the CDCTC and CTC, the 2025 reconciliation law also made changes to two other child-related tax policy provisions: the Employer-Provided Child Care Credit (45F) and the Dependent Care Assistance Plans (DCAP). The Employer-Provided Child Care Credit is a tax credit for employers who provide on-site child care and resource and referral services for employees. It was expanded by increasing the credit rate (up to 40%, or 50% for small businesses) and raising the maximum credit, while also broadening eligible expenses to include third-party and shared child care arrangements. These changes are intended to encourage greater employer investment in child care and expand access to employer-supported options. According to the U.S. Congressional Research Service, the Employer-Provided Child Care Credit has historically had a low utilization rate and minimal impact on expanding child care access and availability.[31]

Additionally, the DCAP, which serves as an employee-sponsored Flexible Spending Account, was enhanced by increasing the amount employees can set aside in pre-tax dollars for child care expenses from $5,000 to $7,500, updating a long-standing but limited benefit.[32] While this change allows more working families to reduce taxable income, access depends on employer participation, meaning benefits are concentrated among workers with employer-sponsored plans. Additionally, enrollment in the DCAP could affect filers with CDCTC eligible credit, as dollars contributed to the DCAP would be ineligible for also being applied to the CDCTC.[33]

Looking Ahead

While child tax credit provisions, such as the CTC and CDCTC, provide an important baseline of support, many states have strengthened their impact by adopting or enhancing assistance to families through state-level changes to eligibility, benefit amounts, and refundability, which can broaden access for families with low and moderate incomes who may otherwise have limited support under current federal child tax structures. However, tax policy represents only one component of a broader strategy for addressing child care affordability and reducing economic barriers for working families. Targeted investment in state level direct assistance programs, such as New Hampshire’s Child Care Scholarship Program and Financial Assistance for Needy Families, can play a critical role in reinforcing the financial safety net for families by reducing the expenses associated with raising children, including the high cost of child care services.[34]

Endnotes

[1] See NHFPI’s August 2025 Issue Brief New Federal Reconciliation Law Reduces Taxes, Health Access, and Food Assistance Supports for Granite Staters.

[2] To read the 2025 reconciliation law, see H.R. 1 – One Big Beautiful Bill Act on the Congress.gov website. To learn more about the reconciliation process, see the U.S. Congressional Research Service’s March 6, 2025 report The Reconciliation Process: Frequently Asked Questions. For more details on Child and Dependent Care Tax Credit eligibility, see the U.S. Internal Revenue Service Publication 503 Child and Dependent Care Expenses. For more details on the Child Tax Credit, see the 2025 U.S. Congressional Research Service report, The Child Tax Credit: How it Works and Who Receives It.

[3] See NHFPI’s 2025 report Affordability Eroded: Changes to the Cost of Living in New Hampshire.

[4] For more details on diaper insecurity in New Hampshire, see Urban Institute data tool, Mapping Diaper Insecurity in the US. For more details on recent changes in diaper insecurity, see National Diaper Bank Network, Diaper Insecurity Harms Maternal Mental Health in the Postpartum Period. For more details on food price increases, see NHFPI’s January 28, 2026 presentation slides on The Cost of Living Over Time and Funding for Public Services in New Hampshire. slide 11. See also Purdue University’s Center for Food Demand Analysis and Sustainability.

[5] Annual cost for child care was calculated using average 2022-2024 annual estimates produced by Child Care Aware of America’s 2022, 2023, and 2024New Hampshire Price of Care Fact Sheets. For customized data extractions, see IPUMS USA, University of Minnesota, 2020-2024 American Community Survey (ACS) 5-Year Data, U.S. Census Bureau online data tool. The following indicators were used to generate the custom table: Total family income, state (FIPS code), marital status, sex, number of own children under age 5 in household, and relationship to household head.

[6] See the 2021 Congressional Research Service report, Child and Dependent Care Tax Benefits: How They Work and Who Receives Them. See also the Tax Policy Center, 2025 Reconciliation Law Makes Some Modest Changes to Child Care Tax Benefits, Provides Little Help For Low-Income Families and the Columbia University Center on Poverty and Social Policy, Children Left Behind: The Child Tax Credit and OBBBA.

[7] See the 2021 Congressional Research Service report, Child and Dependent Care Tax Benefits: How They Work and Who Receives Them. For more details on the Child and Dependent Care Tax Credit, see the Internal Revenue Service Child and Dependent Care Credit Information website. For further details related to eligibility, see Internal Revenue Service Publication 503 Child and Dependent Care Expenses.

[8] See the 2021 Congressional Research Service report, Child and Dependent Care Tax Benefits: How They Work and Who Receives Them.

[9] See the 2021 Congressional Research Service report, Child and Dependent Care Tax Benefits: How They Work and Who Receives Them.

[10] See the Internal Revenue Service Topic no. 602, Child and Dependent Care Credit.

[11] See the 2021 Congressional Research Service report, The Child and Dependent Care Tax Credit (CDCTC): Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021.

[12] For customized data extractions, see IPUMS USA, University of Minnesota, 2020-2024 American Community Survey (ACS) 5-Year Data, U.S. Census Bureau online data tool. The following indicators were used to generate the custom table: Total family income, state (FIPS code), marital status, number of own children under age 5 in household, and relationship to household head.

[13] For customized data extractions, see IPUMS USA, University of Minnesota, 2020-2024 American Community Survey (ACS) 5-Year Data, U.S. Census Bureau online data tool. The following indicators were used to generate the custom table: State (FIPS code), marital status, and age of youngest own child in household.

[14] For customized data extractions, see IPUMS USA, University of Minnesota, 2020-2024 American Community Survey (ACS) 5-Year Data, U.S. Census Bureau online data tool. The following indicators were used to generate the custom table: State (FIPS code), marital status, and number of own children under age 5 in household.

[15] See the U.S. Internal Revenue Service, SOI Tax Stats: Historic Table 2, New Hampshire, 2022.

[16] For customized data extractions, see IPUMS USA, University of Minnesota, 2020-2024 American Community Survey (ACS) 5-Year Data, U.S. Census Bureau online data tool. The following indicators were used to generate the custom tables on race/ethnicity of total eligible children and race/ethnicity of children eligible for 50% CDCTC: State (FIPS code), race and ethnicity, age, total family income, and relationship to household head. See also the Tax Policy Center, 2025 Reconciliation Law Makes Some Modest Changes to Child Care Tax Benefits, Provides Little Help For Low-Income Families.

[17] See the Tax Policy Center, 2025 Reconciliation Law Makes Some Modest Changes to Child Care Tax Benefits, Provides Little Help For Low-Income Families.

[18] See the 2025 U.S. Congressional Research Service report, The Child Tax Credit: How it Works and Who Receives It.

[19] See the U.S. Internal Revenue Service, Child Tax Credit website.

[20] See NHFPI’s March 2022 Issue Brief on the Expansions of the Earned Income Tax Credit and Child Tax Credit in New Hampshire.

[21] See NHFPI’s April 2024 Data Byte titled Supplemental Poverty Measure Indicates Child Poverty Rebounded in New Hampshire During 2022. See also the U.S. Census Bureau 2022 report on The Impact of the 2021 Expanded Child Tax Credit on Child Poverty. The measure of poverty used for these calculations was the federal Supplemental Poverty Measure, which is separate from the Official Poverty Measure that focuses on pre-tax income. Tax credits are delivered through the tax code, and are thus not considered pre-tax income.

[22] See the 2025 U.S. Congressional Research Service report, The Child Tax Credit: How it Works and Who Receives It.

[23] See Columbia University Center on Poverty and Social Policy, Children Left Behind: The Child Tax Credit and OBBBA.

[24] See the U.S. Internal Revenue Service, Child Tax Credit website.

[25] See Columbia University Center on Poverty and Social Policy, Children Left Behind: The Child Tax Credit and OBBBA.

[26] See the Institute on Taxation and Economic Policy 2026 report, The Child Tax Credit Leaves Out Millions of Children in 2026. There are Better Alternatives.

[27] See the 2025 U.S. Congressional Research Service report, The Child Tax Credit: How it Works and Who Receives It.

[28] See the Columbia University Center on Poverty and Social Policy’s August 6, 2025 brief Children Left Behind by the H.R.1

“One Big Beautiful Bill Act” Child Tax Credit.

[29] The $984,000 was calculated using available 2020-2024 U.S. Census Bureau Five-Year American Community Survey (ACS) data indicators on New Hampshire family’s marital status, number of children in household under seventeen years of age, and family income. Using these data and the 2024 and 2025 CTC full credit rate, we calculated the estimated difference in loss of returns families with an income between $25,000-38,000 could experience. See the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation report on Health Care and Child Care Costs Contribute to the Unsustainable and Growing Cost of Raising a Family in America. See also Columbia University’s Center on Poverty and Social Policy, Children Left Behind: The Child Tax Credit and OBBBA.

[30] See the Internal Revenue Service, SOI Tax Stats: Historic Table 2, New Hampshire, 2022.

[31] See the U.S. Congressional Research Service 2025 report on the 45F Tax Credit for Employer-Provided Child care. See also the Child Care Aware of America 2025 blog titled Final Reconciliation Package Improves Child Care Tax Credits, Deeply Cuts Other Programs—Ultimately Harming Millions of Children and Families and the Tax Policy Center’s 2025 Reconciliation Law Makes Some Modest Changes to Child Care Tax Benefits, Provides Little Help For Low-Income Families.

[32] See the U.S. Congressional Research Service’s 2025 report about the 45F Tax Credit for Employer-Provided Child care, the Child Care Aware of America 2025 blog titled Final Reconciliation Package Improves Child Care Tax Credits, Deeply Cuts Other Programs—Ultimately Harming Millions of Children and Families, and the Tax Policy Center’s 2025 Reconciliation Law Makes Some Modest Changes to Child Care Tax Benefits, Provides Little Help For Low-Income Families.

[33] See the 2021 U.S. Congressional Research Service report, Child and Dependent Care Tax Benefits: How They Work and Who Receives Them.

[34] See the Bipartisan Policy Center report on State Tax Policies for Working Parents. See the W.E. Upjohn Institute for Employment Research 2026 report on Three Ways States Can Build a Better Child and Dependent Care Tax Credit. See also the Center on Budget and Policy Priorities March 2023 report, States Enact or Expand Child Tax Credits and Earned Income Tax Credits to Build Equitable, Inclusive Communities and Economies, NHFPI’s 2026 blog on Child Care Scholarships Reach More Families as Potential Funding Challenges Loom, and NHFPI’s July 2024 blog Under Enrollment in Key Aid Program and Increased Available Funds Provide Opportunities for Enhanced Outreach and Assistance.

The New Hampshire Fiscal Policy Institute is sharing these articles with the partners in The Granite State News Collaborative. NHFPI is an independent nonprofit organization that explores, develops and promotes public policies that foster economic opportunity and prosperity for all New Hampshire residents. For more information visit nhfpi.org. These articles are being shared by partners in The Granite State News Collaborative. For more information visit collaborativenh.org.