KEY POINTS

-

- After a long period of declines, key State revenues may be recovering

- The one-time Tax Amnesty Program and ongoing State revenue sources have helped finances this year

- Business tax revenues rebounded in April, and this year’s refunds are lower

- Taxes paid based on this year’s business activity do not indicate ongoing growth is guaranteed

- Revenues continue to be diminished by smaller State cash holdings and the Interest and Dividends Tax repeal

- Insurance Premium Tax revenues continue to consistently outperform official projections

- Real Estate Transfer Tax revenues, which slid with the lack of housing inventory and sales, are recovering

- Video Lottery Terminals are underperforming targets, but are being offset by higher earnings from the rest of Lottery Commission activities

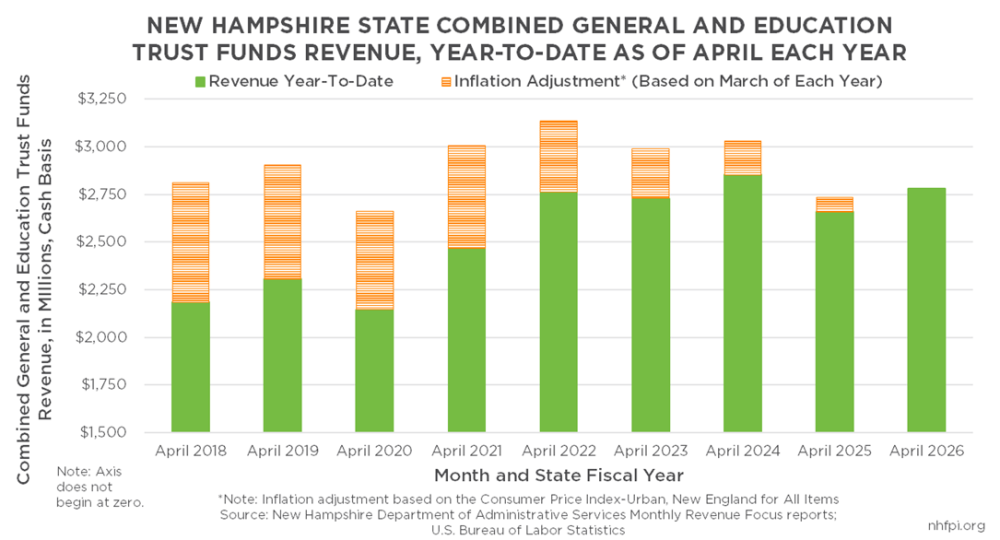

- As of the end of April, inflation-adjusted General and Education Trust Funds revenues are lower than they were in six of the last eight years

State revenue collections in April, which is the most important month for the year for State tax receipts, offered key insights into current State finances and potential revenue trends for the rest of the State Budget biennium. With only two months left in State Fiscal Year (SFY) 2026 which began July 1, 2025 and ends on June 30 of this calendar year, the State has a healthy revenue surplus. While key unexpected costs may arise, the State appears to have enough revenue to pay for budgeted expenditures this year, which was not a certainty based on revenues from earlier in SFY 2026.

The State of New Hampshire’s one-time Tax Amnesty Program has been the most important generator of revenue surplus. However, revenue growth from combined business tax returns, rebounding Real Estate Transfer Tax receipts, and growing lottery and Insurance Premium Tax revenues have all boosted the State’s finances. While these trends have helped, key signs in the business tax revenues hint that an extended rebound is not guaranteed, and underperformance in Video Lottery Terminals, lower interest payments generated by State cash holdings, and the repeal of the Interest and Dividends Tax continue to weigh on State revenues.

Analysis of revenues coming into the State’s General Fund and Education Trust Fund, two primary State Budget funds that share several key tax revenue sources, suggest that this upturn in receipts may signal the end of a long-term slide in State revenues, but that revenues have not recovered fully and remain more limited in their overall ability to fund public services than they were in six of the last eight years.[1] Here are ten takeaways from April’s State revenues.

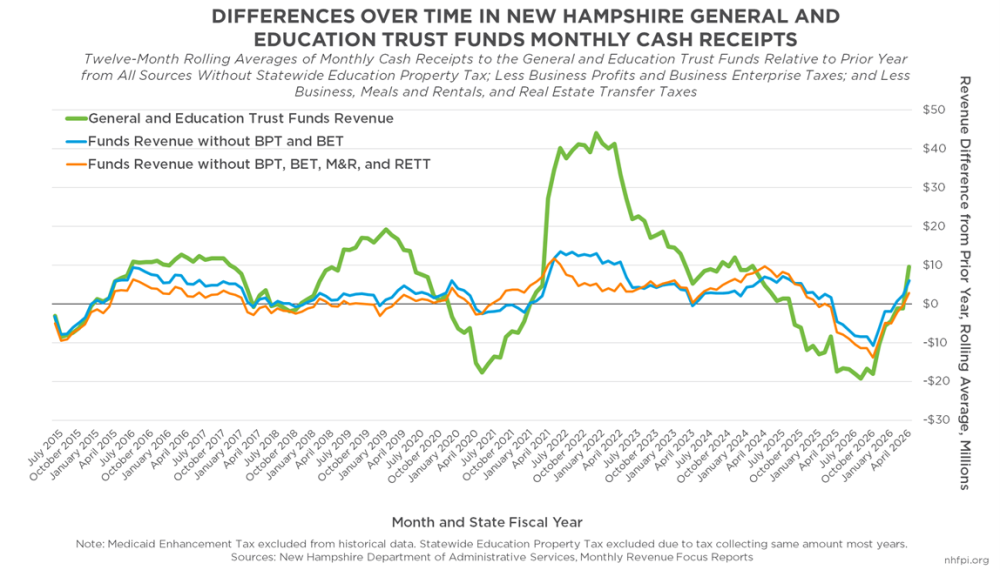

1. After a Long Decline, State Revenues May Have Started Recovering

After nearly two years of State revenues commonly falling behind their comparable collections from the year before, revenues have started growing again. Of the 34 months from July 2024, the start of the prior biennial State Budget, to April 2026, 20 months (58.8%) had revenues falling short of the collections from the previous year for the combined General and Education Trust Funds.[2]

The result was lower General Fund and Education Trust Fund revenues in SFY 2025 than in either SFYs 2024 or 2023, and revenues that fell short of amounts targeted in the State Revenue Plan, which is based on State Budget projections, as well.[3]

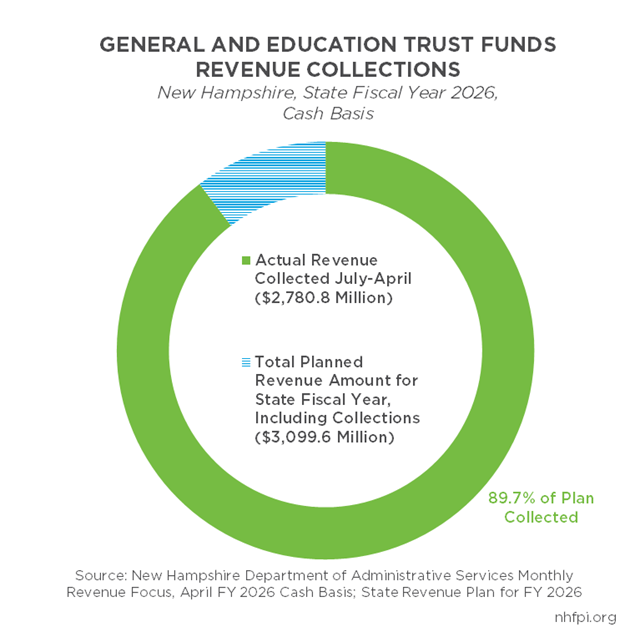

As of the end of April, State revenue collected for the General and Education Trust Funds for SFY 2026 thus far were above last year’s receipts through April by $121.5 million (4.6%). These revenues also exceeded the State Revenue Plan’s target collections for the year thus far by $154.3 million (5.9%).[4]

In September SFY 2025, average cash-basis revenue for the General and Education Trust Funds for the prior 12 months was below the period covering the 12 months of the year before. That 12-month rolling average deficit increased over time, and the average monthly shortfall for a 12-month period peaked at $19.2 million in August SFY 2026; this figure indicates that, during the average month in the year ending last August, the State collected $19.2 million less every month, on average, than it did in the 12 months ending August of the year before.

However, the fortunes of State revenues have recovered since that time. The average 12-month rolling deficit shrank during most months since August. In April SFY 2026, average monthly revenues over the prior year were positive compared to the year before for the first time since September SFY 2025.

In summary, revenues have started growing again after falling behind previous years for well over half of a State Budget cycle.

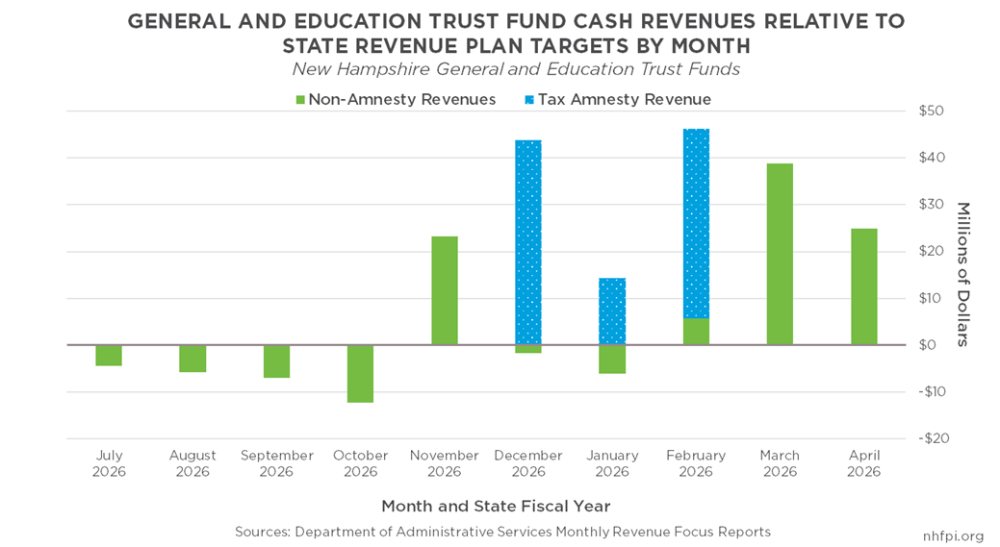

2. One-Time Tax Amnesty Has Helped, But Is Not the Whole Story

The primary reason the State currently has a revenue surplus over the State Revenue Plan in SFY 2026 thus far is the State’s Tax Amnesty Program. The Tax Amnesty Program allowed individuals and businesses with unpaid taxes to pay past-due amounts without the nonpayment penalties that the State typically charges, and permitted 50% lower interest costs due to the later payments than typically would be charged. The Program, which was established by the State Budget and ran from December 1 to February 15, was projected to generate $5.0 million for the combined General and Education Trust Funds in the Legislature’s forecasting.[5]

Instead, this cost-saving measure for people and businesses with overdue and unpaid taxes brought in $103.8 million during its short existence, or nearly 21 times the amount of revenue the Legislature forecast when making State Budget projections. While not all tax revenue sources flow to the State’s General and Education Trust Funds, all revenue paid through the Tax Amnesty Program flowed to these two funds.[6]

This additional one-time revenue was deposited in State coffers in December, January, and February, and the rest of State revenue sources from other, ongoing sources ended February in a deficit for SFY 2026 to date.[7] However, March and April revenues from other sources since the Program’s end have pushed the rest of the State revenue picture back into surplus.

Removing the Tax Amnesty Program revenues, State General and Education Trust Funds receipts were still $55.5 million (2.1%) ahead of planned amounts for this point in SFY 2026, and $17.7 million (0.7%) ahead of last year’s receipts to date. The Tax Amnesty program is critical to the overall revenue surplus of $154.3 million (5.9%) as of the end of April, but other sources, most notably rebounding business tax revenues, have helped support a revenue surplus as well.

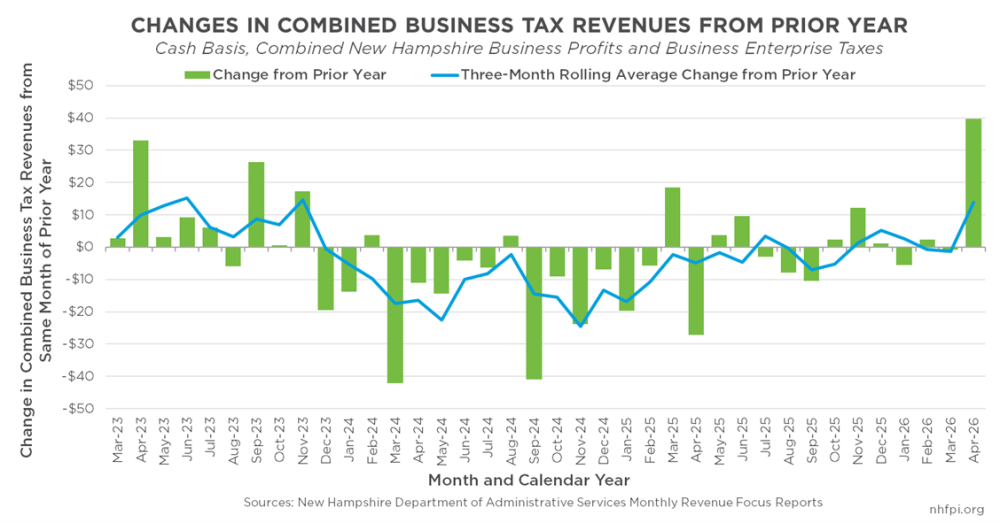

3. Topline Business Taxes Revenues Rebounded

Combined revenues from the State’s Business Profits Tax and Business Enterprise Tax, which are reported together in monthly cash analyses, had been a primary driver of the State’s recent string of monthly revenue shortfalls. Last fiscal year, the Business Profits Tax and Business Enterprise Tax were the State’s largest and fifth-largest tax revenue sources, respectively, for the New Hampshire State government. Combined business tax revenues were $130.1 million (10.6%) lower in SFY 2025 than in SFY 2024, and $163.4 million (13.0%) below the State Revenue Plan’s target for that year. That drop followed a $33.2 million (2.6%) decline in these revenues between SFYs 2023 and 2024 as well.[8]

However, business tax revenues have strengthened since the first quarter of SFY 2026, and grew relative to the prior year in five of the last seven months since September. This growth was not robust, and did not fully offset the shortfall from the first quarter of the year; as of the end of March, business tax revenues were still $9.6 million (1.5%) below the revenue that had been collected from those two taxes by March of the previous year, and they were $32.5 million (4.8%) below the targeted amount year-to-date.[9]

However, April revenues altered the growth trajectory. In April, combined business tax revenues were $26.1 million (10.3%) above the State Revenue Plan target for the month and $39.8 million (16.6%) ahead of the prior year. Even with this bump, business tax revenue collections for the full year thus far were still below planned amounts by $6.4 million (0.7%). However, the 3.4% year-over-year growth, comparing receipts year-to-date for April of this year to last year, provides a potential boost to the future prospects for State revenue overall after the performance of the business taxes had dragged State finances below targets earlier in the year.

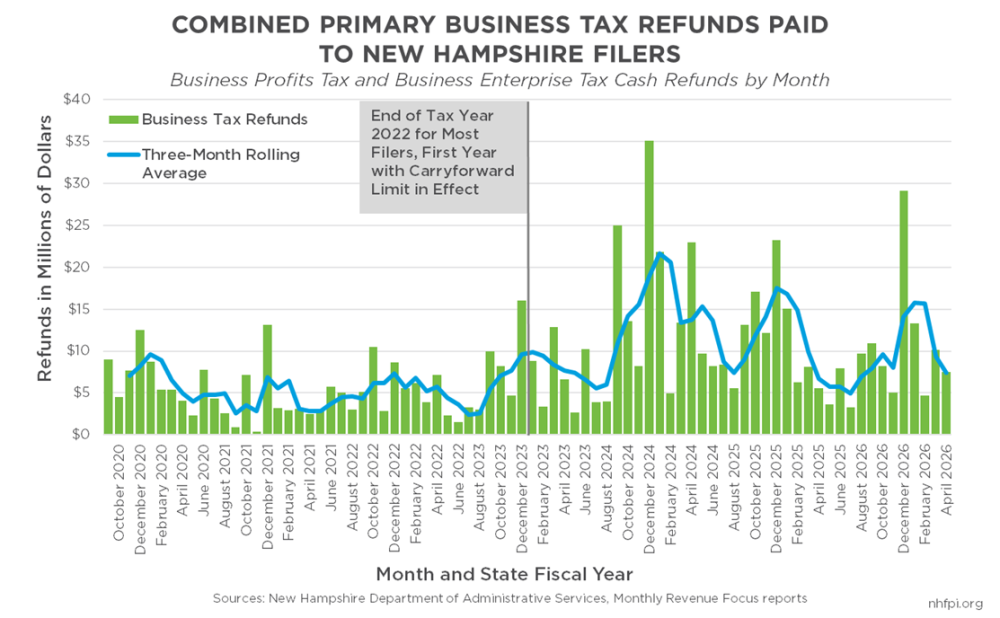

4. Business Tax Refunds are Still Elevated, but Falling

If they are beginning to grow again, business tax revenues are likely doing so for a variety of reasons. These reasons could range from higher corporate profits to boosts in payroll to a higher percentage of multi-state and multi-national sales for some companies being based in New Hampshire than in previous years.

One measurable reason why revenues may be increasing is a long-term reduction in requests for refunds. Businesses that overpay their taxes may request refunds from the State, and these refunds lower the amount of net revenue the State receives through business taxes.

Refunds have increased since 2023, in part due to State policy changes. Starting in Tax Year 2022, State policymakers capped the amount of money a business taxpayer can hold, or carryforward, as credit with the State to 500 percent of its liability, and the rest must be refunded; that carryforward cap will drop to 250 percent of tax liability in Tax Year 2029 under current law. The cap appeared to result in increased refunds requested, as businesses that otherwise may have stored their money with the State, which does pay interest, were required to shift their dollars elsewhere.[10]

The cap, which started in Tax Year 2022, likely had the greatest impact on SFYs 2023 and 2024 revenues as businesses adjusted to the new limitation. Year-to-date business tax refunds as of the end of April SFY 2026 totaled $101.8 million, which was $51.1 million (33.4%) less than the same time in SFY 2024, which was the year business tax refunds peaked.[11]

With the one-time impact of imposing a new cap on credit carryforward fading, net business tax revenues may be higher again after a period during which businesses were required to take more refunds from the State.

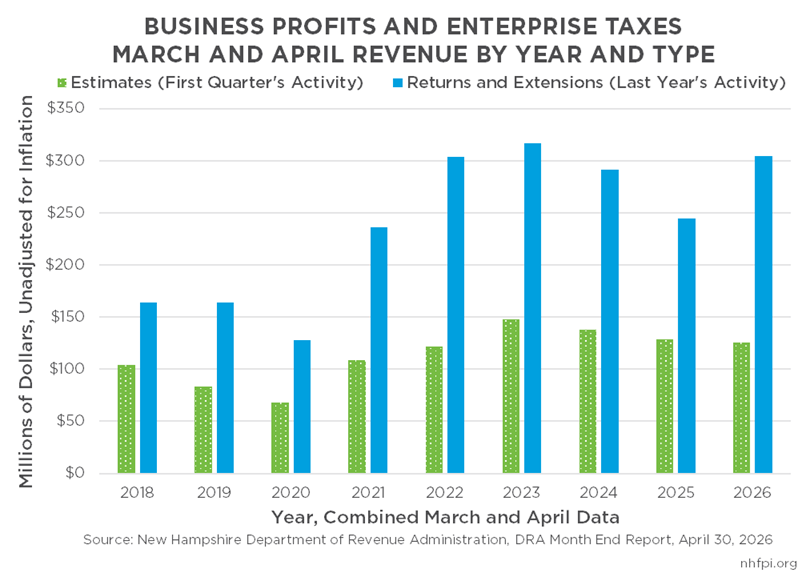

5. Business Taxes Higher Due to Last Year’s Activity, Not This Year’s Economy

March and April are key months for business tax revenues because they include two types of payment for most businesses. The majority of business tax revenue is paid through quarterly estimate payments that businesses pay every three or four months within their tax year, reflecting their projected tax liability based on the activity of the prior quarter. As the State reports that about 90 percent of businesses have a tax year that matches the calendar year, the months of June, September, December, and then March and April combined are key months for State revenue overall due to these quarterly payments in business taxes.

March and April, however, are particularly important because businesses that have a tax year matching the calendar year also owe their returns from the previous year on those months. Partnership returns for the prior year, as well as the first quarterly estimate payments for the new year, are due in March for those businesses, and all other business types have their returns and first quarter estimate payments due in April. If these businesses do not file their full return by the March or April due dates, they may file extensions, but must include their full payments in those extensions.[12]

As a result, March and April receipts provide insight into both how economic activity fared in the prior year relative to the amount paid in quarterly estimate payments last year already, as well as business experiences from the first quarter of a new year.

Receipts from March and April of this year suggest that businesses may have done better than they projected they would when paying quarterly estimates last year. Combined returns and extensions were $60.0 million (24.6%) higher in March and April this year than the same months in SFY 2025, and were the highest, unadjusted for inflation, that they have been for these two months since their peak in SFY 2023. Those returns send a signal that, potentially, businesses had a higher tax liability than they expected when tracking profits and other taxable activity throughout the year.[13]

The estimate payments due in March and April, however, provide less reason to forecast growth in the current-day economy. Estimate payments were $3.5 million (2.7%) lower in March and April SFY 2026 than they were in the same months in SFY 2025, and were $22.2 million (15.0%) below the comparable data for the SFY 2023 peak. While revenues can change quickly and have done so in the past, this set of estimate collections falling below any year since SFY 2022, without an inflation adjustment, suggests businesses are less optimistic about the economy in the first quarter than they have been in recent years.

6. Two Key Sources from Prior Years Waning

Revenue from sources beyond the State’s two primary business taxes also had significant impacts on State receipts in March and April. While some revenue sources continue to show long-term growth, the two sources that were almost entirely responsible for the State’s revenue surplus in SFY 2024 have been substantially diminished over the last two years.

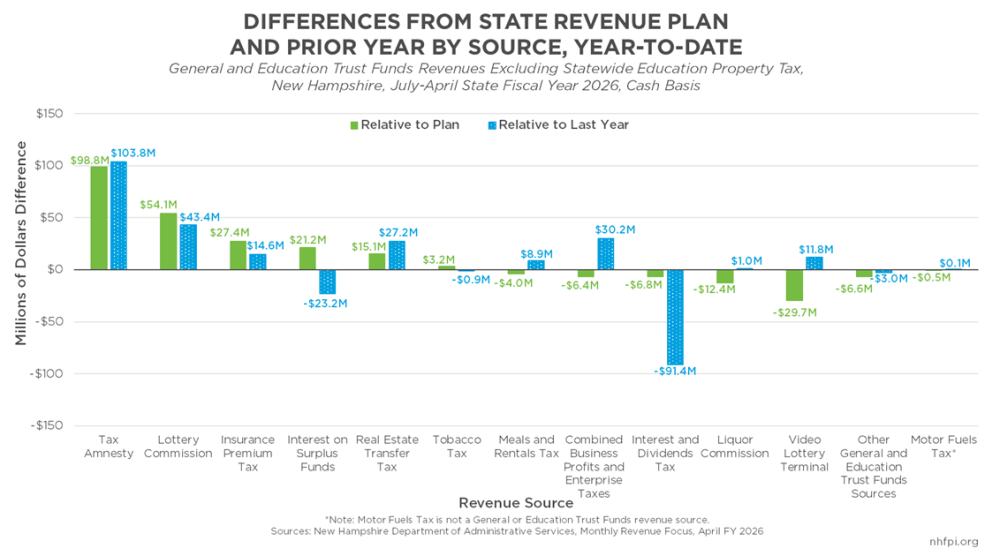

First, interest on State cash holdings has generated significant unplanned surpluses since SFY 2024 as the State government held revenue from prior surpluses and one-time, temporary federal funds. While these revenues are still ahead of planned amounts so far this year, at $21.2 million (48.0%) ahead of the State Revenue Plan target, these revenues are $23.2 million (26.2%) behind last year’s totals. These revenues will likely continue to fall behind as the State spends down cash holdings from both one-time federal aid and prior surpluses.[14]

Second, the 2025 repeal of the Interest and Dividends Tax continues to push State revenue lower than it was in previous years. The Interest and Dividends Tax was levied on income derived from wealth, such as dividends and distributions from business ownership.[15] The multi-year phaseout and subsequent full repeal of this tax has resulted in substantially lower revenues, including a $91.4 million drop as of the end of April SFY 2026 relative to last year.

Other revenue sources were a mixed picture, with a few key trends driving longer-term revenue changes. These trends include growing Insurance Premium Tax revenues, a nearly rebounded Real Estate Transfer Tax, and mixed trajectories among expanded gambling options.

KEY POINTS

-

- After a long period of declines, key State revenues may be recovering

- The one-time Tax Amnesty Program and ongoing State revenue sources have helped finances this year

- Business tax revenues rebounded in April, and this year’s refunds are lower

- Taxes paid based on this year’s business activity do not indicate ongoing growth is guaranteed

- Revenues continue to be diminished by smaller State cash holdings and the Interest and Dividends Tax repeal

- Insurance Premium Tax revenues continue to consistently outperform official projections

- Real Estate Transfer Tax revenues, which slid with the lack of housing inventory and sales, are recovering

- Video Lottery Terminals are underperforming targets, but are being offset by higher earnings from the rest of Lottery Commission activities

- As of the end of April, inflation-adjusted General and Education Trust Funds revenues are lower than they were in six of the last eight years

State revenue collections in April, which is the most important month for the year for State tax receipts, offered key insights into current State finances and potential revenue trends for the rest of the State Budget biennium. With only two months left in State Fiscal Year (SFY) 2026 which began July 1, 2025 and ends on June 30 of this calendar year, the State has a healthy revenue surplus. While key unexpected costs may arise, the State appears to have enough revenue to pay for budgeted expenditures this year, which was not a certainty based on revenues from earlier in SFY 2026.

The State of New Hampshire’s one-time Tax Amnesty Program has been the most important generator of revenue surplus. However, revenue growth from combined business tax returns, rebounding Real Estate Transfer Tax receipts, and growing lottery and Insurance Premium Tax revenues have all boosted the State’s finances. While these trends have helped, key signs in the business tax revenues hint that an extended rebound is not guaranteed, and underperformance in Video Lottery Terminals, lower interest payments generated by State cash holdings, and the repeal of the Interest and Dividends Tax continue to weigh on State revenues.

Analysis of revenues coming into the State’s General Fund and Education Trust Fund, two primary State Budget funds that share several key tax revenue sources, suggest that this upturn in receipts may signal the end of a long-term slide in State revenues, but that revenues have not recovered fully and remain more limited in their overall ability to fund public services than they were in six of the last eight years.[1] Here are ten takeaways from April’s State revenues.

1. After a Long Decline, State Revenues May Have Started Recovering

After nearly two years of State revenues commonly falling behind their comparable collections from the year before, revenues have started growing again. Of the 34 months from July 2024, the start of the prior biennial State Budget, to April 2026, 20 months (58.8%) had revenues falling short of the collections from the previous year for the combined General and Education Trust Funds.[2]

The result was lower General Fund and Education Trust Fund revenues in SFY 2025 than in either SFYs 2024 or 2023, and revenues that fell short of amounts targeted in the State Revenue Plan, which is based on State Budget projections, as well.[3]

As of the end of April, State revenue collected for the General and Education Trust Funds for SFY 2026 thus far were above last year’s receipts through April by $121.5 million (4.6%). These revenues also exceeded the State Revenue Plan’s target collections for the year thus far by $154.3 million (5.9%).[4]

In September SFY 2025, average cash-basis revenue for the General and Education Trust Funds for the prior 12 months was below the period covering the 12 months of the year before. That 12-month rolling average deficit increased over time, and the average monthly shortfall for a 12-month period peaked at $19.2 million in August SFY 2026; this figure indicates that, during the average month in the year ending last August, the State collected $19.2 million less every month, on average, than it did in the 12 months ending August of the year before.

However, the fortunes of State revenues have recovered since that time. The average 12-month rolling deficit shrank during most months since August. In April SFY 2026, average monthly revenues over the prior year were positive compared to the year before for the first time since September SFY 2025.

In summary, revenues have started growing again after falling behind previous years for well over half of a State Budget cycle.

2. One-Time Tax Amnesty Has Helped, But Is Not the Whole Story

The primary reason the State currently has a revenue surplus over the State Revenue Plan in SFY 2026 thus far is the State’s Tax Amnesty Program. The Tax Amnesty Program allowed individuals and businesses with unpaid taxes to pay past-due amounts without the nonpayment penalties that the State typically charges, and permitted 50% lower interest costs due to the later payments than typically would be charged. The Program, which was established by the State Budget and ran from December 1 to February 15, was projected to generate $5.0 million for the combined General and Education Trust Funds in the Legislature’s forecasting.[5]

Instead, this cost-saving measure for people and businesses with overdue and unpaid taxes brought in $103.8 million during its short existence, or nearly 21 times the amount of revenue the Legislature forecast when making State Budget projections. While not all tax revenue sources flow to the State’s General and Education Trust Funds, all revenue paid through the Tax Amnesty Program flowed to these two funds.[6]

This additional one-time revenue was deposited in State coffers in December, January, and February, and the rest of State revenue sources from other, ongoing sources ended February in a deficit for SFY 2026 to date.[7] However, March and April revenues from other sources since the Program’s end have pushed the rest of the State revenue picture back into surplus.

Removing the Tax Amnesty Program revenues, State General and Education Trust Funds receipts were still $55.5 million (2.1%) ahead of planned amounts for this point in SFY 2026, and $17.7 million (0.7%) ahead of last year’s receipts to date. The Tax Amnesty program is critical to the overall revenue surplus of $154.3 million (5.9%) as of the end of April, but other sources, most notably rebounding business tax revenues, have helped support a revenue surplus as well.

3. Topline Business Taxes Revenues Rebounded

Combined revenues from the State’s Business Profits Tax and Business Enterprise Tax, which are reported together in monthly cash analyses, had been a primary driver of the State’s recent string of monthly revenue shortfalls. Last fiscal year, the Business Profits Tax and Business Enterprise Tax were the State’s largest and fifth-largest tax revenue sources, respectively, for the New Hampshire State government. Combined business tax revenues were $130.1 million (10.6%) lower in SFY 2025 than in SFY 2024, and $163.4 million (13.0%) below the State Revenue Plan’s target for that year. That drop followed a $33.2 million (2.6%) decline in these revenues between SFYs 2023 and 2024 as well.[8]

However, business tax revenues have strengthened since the first quarter of SFY 2026, and grew relative to the prior year in five of the last seven months since September. This growth was not robust, and did not fully offset the shortfall from the first quarter of the year; as of the end of March, business tax revenues were still $9.6 million (1.5%) below the revenue that had been collected from those two taxes by March of the previous year, and they were $32.5 million (4.8%) below the targeted amount year-to-date.[9]

However, April revenues altered the growth trajectory. In April, combined business tax revenues were $26.1 million (10.3%) above the State Revenue Plan target for the month and $39.8 million (16.6%) ahead of the prior year. Even with this bump, business tax revenue collections for the full year thus far were still below planned amounts by $6.4 million (0.7%). However, the 3.4% year-over-year growth, comparing receipts year-to-date for April of this year to last year, provides a potential boost to the future prospects for State revenue overall after the performance of the business taxes had dragged State finances below targets earlier in the year.

4. Business Tax Refunds are Still Elevated, but Falling

If they are beginning to grow again, business tax revenues are likely doing so for a variety of reasons. These reasons could range from higher corporate profits to boosts in payroll to a higher percentage of multi-state and multi-national sales for some companies being based in New Hampshire than in previous years.

One measurable reason why revenues may be increasing is a long-term reduction in requests for refunds. Businesses that overpay their taxes may request refunds from the State, and these refunds lower the amount of net revenue the State receives through business taxes.

Refunds have increased since 2023, in part due to State policy changes. Starting in Tax Year 2022, State policymakers capped the amount of money a business taxpayer can hold, or carryforward, as credit with the State to 500 percent of its liability, and the rest must be refunded; that carryforward cap will drop to 250 percent of tax liability in Tax Year 2029 under current law. The cap appeared to result in increased refunds requested, as businesses that otherwise may have stored their money with the State, which does pay interest, were required to shift their dollars elsewhere.[10]

The cap, which started in Tax Year 2022, likely had the greatest impact on SFYs 2023 and 2024 revenues as businesses adjusted to the new limitation. Year-to-date business tax refunds as of the end of April SFY 2026 totaled $101.8 million, which was $51.1 million (33.4%) less than the same time in SFY 2024, which was the year business tax refunds peaked.[11]

With the one-time impact of imposing a new cap on credit carryforward fading, net business tax revenues may be higher again after a period during which businesses were required to take more refunds from the State.

5. Business Taxes Higher Due to Last Year’s Activity, Not This Year’s Economy

March and April are key months for business tax revenues because they include two types of payment for most businesses. The majority of business tax revenue is paid through quarterly estimate payments that businesses pay every three or four months within their tax year, reflecting their projected tax liability based on the activity of the prior quarter. As the State reports that about 90 percent of businesses have a tax year that matches the calendar year, the months of June, September, December, and then March and April combined are key months for State revenue overall due to these quarterly payments in business taxes.

March and April, however, are particularly important because businesses that have a tax year matching the calendar year also owe their returns from the previous year on those months. Partnership returns for the prior year, as well as the first quarterly estimate payments for the new year, are due in March for those businesses, and all other business types have their returns and first quarter estimate payments due in April. If these businesses do not file their full return by the March or April due dates, they may file extensions, but must include their full payments in those extensions.[12]

As a result, March and April receipts provide insight into both how economic activity fared in the prior year relative to the amount paid in quarterly estimate payments last year already, as well as business experiences from the first quarter of a new year.

Receipts from March and April of this year suggest that businesses may have done better than they projected they would when paying quarterly estimates last year. Combined returns and extensions were $60.0 million (24.6%) higher in March and April this year than the same months in SFY 2025, and were the highest, unadjusted for inflation, that they have been for these two months since their peak in SFY 2023. Those returns send a signal that, potentially, businesses had a higher tax liability than they expected when tracking profits and other taxable activity throughout the year.[13]

The estimate payments due in March and April, however, provide less reason to forecast growth in the current-day economy. Estimate payments were $3.5 million (2.7%) lower in March and April SFY 2026 than they were in the same months in SFY 2025, and were $22.2 million (15.0%) below the comparable data for the SFY 2023 peak. While revenues can change quickly and have done so in the past, this set of estimate collections falling below any year since SFY 2022, without an inflation adjustment, suggests businesses are less optimistic about the economy in the first quarter than they have been in recent years.

6. Two Key Sources from Prior Years Waning

Revenue from sources beyond the State’s two primary business taxes also had significant impacts on State receipts in March and April. While some revenue sources continue to show long-term growth, the two sources that were almost entirely responsible for the State’s revenue surplus in SFY 2024 have been substantially diminished over the last two years.

First, interest on State cash holdings has generated significant unplanned surpluses since SFY 2024 as the State government held revenue from prior surpluses and one-time, temporary federal funds. While these revenues are still ahead of planned amounts so far this year, at $21.2 million (48.0%) ahead of the State Revenue Plan target, these revenues are $23.2 million (26.2%) behind last year’s totals. These revenues will likely continue to fall behind as the State spends down cash holdings from both one-time federal aid and prior surpluses.[14]

Second, the 2025 repeal of the Interest and Dividends Tax continues to push State revenue lower than it was in previous years. The Interest and Dividends Tax was levied on income derived from wealth, such as dividends and distributions from business ownership.[15] The multi-year phaseout and subsequent full repeal of this tax has resulted in substantially lower revenues, including a $91.4 million drop as of the end of April SFY 2026 relative to last year.

Other revenue sources were a mixed picture, with a few key trends driving longer-term revenue changes. These trends include growing Insurance Premium Tax revenues, a nearly rebounded Real Estate Transfer Tax, and mixed trajectories among expanded gambling options.

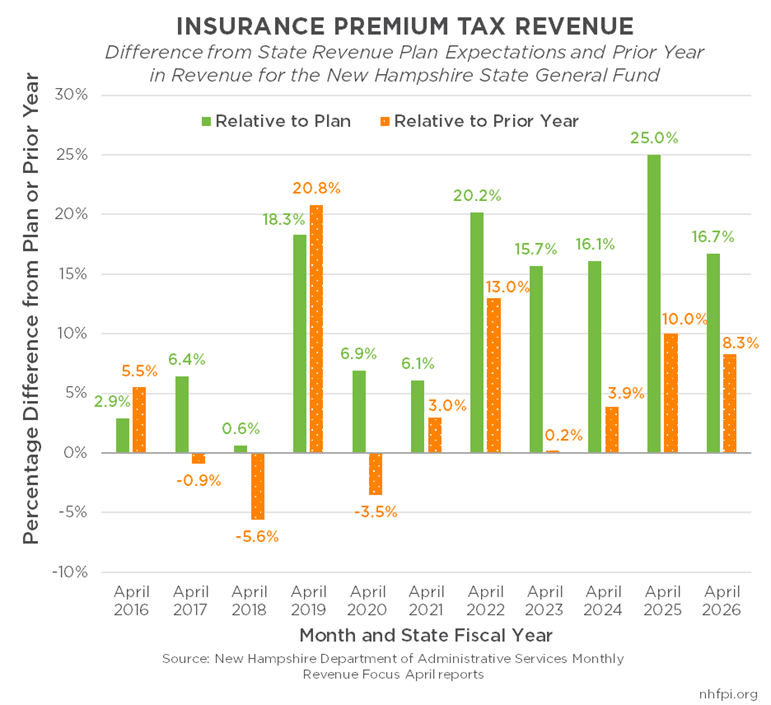

7. Insurance Premium Tax Revenues Continue to Far Exceed Projections

Revenues from the Insurance Premium Tax were a substantial boost for revenues in March, which is in line with recent behavior. The Insurance Premium Tax is based on net premiums charged by insurance companies, which pay the tax directly. Most types of insurance have a 1.25 percent tax rate, but health, accident, and certain other insurers pay at a 2 percent rate.[16]

Insurance Premium Tax revenue, most of which is paid in March of each year, has been much stronger than planned by the State in SFY 2026.[17] Receipts thus far in SFY 2026 were $27.4 million (16.7%) above target and $14.3 million (8.3%) above prior year collections as of the end of April, boosted by receipts that were $28.8 million above target in March alone.

The Insurance Premium Tax is becoming more important for State revenues overall, and State projections for the amount of money that will be generated by this tax each year have consistently underestimated actual revenue in the last decade.[18] While revenue had been ahead of the State Revenue Plan relatively modestly prior to the COVID-19 pandemic, revenue projections since then have been well behind eventual collections. From SFYs 2021 to 2025, General Fund revenue collected from the Insurance Premium Tax exceeded planned amounts by a total of $111.4 million (16.4%), which is equivalent to about 80.2% of the actual total General Fund revenue generated by the Insurance Premium Tax in SFY 2021.

8. Real Estate Transfer Tax Revenues Have Nearly Returned to Post-Pandemic Peak

The Real Estate Transfer Tax is paid by both the buyer and the seller of a property, or interest in a property, and is driven largely by single-family house sales. Increases in housing market prices over the last decade, including both prior to and following the start of the COVID-19 pandemic, boosted Real Estate Transfer Tax revenues considerably. Housing sale prices climbed, and volume was also robust in the immediate aftermath of the pandemic. The subsequent revenue increase from this tax was the second-largest driver of State revenue growth between 2019 and 2022, following revenue growth from the combined business taxes.[19]

![]()

However, revenues started to fall substantially in 2022 as the state’s housing shortage, high prices, and relatively high interest rates reduced the number of sales. Revenues reached their lowest post-pandemic point in SFY 2024, but have climbed slowly since that time as house prices have continued to climb while the overall housing shortage has become slightly less severe.[20]

Real Estate Transfer Tax revenue has nearly recovered to its pre-pandemic peak, without adjusting for inflation. April receipts, which were based on March transactions, were ahead of target by $7.2 million (52.9%) and were $7.9 million (61.2%) higher than last year’s April collections. Those receipts brought the 12-month total for Real Estate Transfer Tax revenues to $228.2 million, which was the highest 12-month total since December SFY 2023 and only $10.9 million short of the 12-month peak of $239.1 million in October SFY 2023.

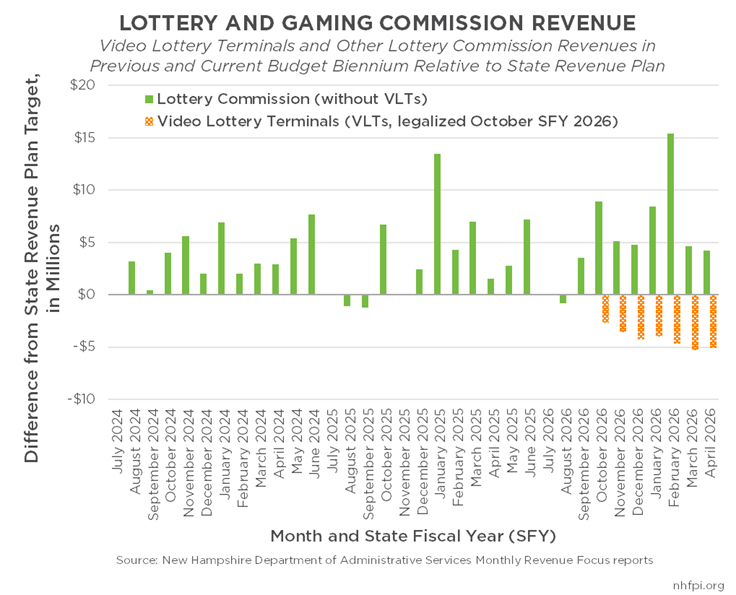

9. Lottery Revenues Luck Split Between Old and New Sources

The Lottery and Gaming Commission generates revenue from legalized gambling, with the profits going to the State primarily for funding local public education. Lottery revenues have grown significantly in the last decade. In SFY 2016, when racing and charitable gaming activities were incorporated into the State Lottery Commission’s purview, the Lottery Commission reported total sales and other revenue of $308.6 million. By SFY 2025, total revenue was $295.8 million (95.8%) higher, at $604.4 million, which itself was a decrease from an even higher level the prior year. Expansions of legal gaming activities that have helped generate this revenue increase between 2017 to 2025 included Keno, the internet-based iLottery and mobile lottery, sports betting, and both higher ticket price and wager caps.[21]

These expanded gaming opportunities, as well as more activity in traditional lottery revenue streams, continue to push revenue up. In April alone, Lottery and Gaming Commission revenues were $4.2 million (28.5%) above planned amounts and above the prior year by $4.5 million (28.1%). For SFY 2026 thus far, Lottery Commission revenues were $54.1 million (37.2%) ahead of the State Revenue Plan’s target and were $43.4 million (27.8%) ahead of last year.

However, the newest component of revenues from the Lottery and Gaming Commission is not performing nearly as well as expected. Video Lottery Terminals, which are reported separately, were legalized for the first time in SFY 2026. These machines have not generated revenue as quickly as anticipated, falling well behind projections in each month and partially offsetting the revenue surplus generated by the rest of the Lottery and Gaming Commission’s revenues. Video Lottery Terminals have generated $29.7 million (71.6%) less than the amounts incorporated into the State Revenue Plan thus far in SFY 2026.

10. Signs of Spring, but Not Yet Summer, for State Revenues

While April receipts brought positive signs for the General and Education Trust Funds, overall State revenues are still diminished relative to prior years. Comparing end-of-April cash receipts across years, General and Education Trust Funds revenues in SFY 2026 are still lower (by 2.6%) than they were in SFY 2024, and only slightly higher (by 0.6%) than the comparable level in SFY 2022.[22]

Adjusting relative to consumer inflation in New England gives an indication as to how the ability of the State government to fund public services from these revenue sources has changed over time.[23] Once adjusted for inflation, year-to-date revenue in SFY 2026 is higher than in SFY 2025, but is lower than every other years since SFY 2018 except for the pandemic-impacted revenue in SFY 2020. While State revenues may be beginning to rebound, they have a significant amount to climb before they return to the inflation-adjusted highs in the years immediately following the COVID-19 pandemic, particularly as the repeal of the Interest and Dividends Tax has eliminated a key State revenue source.

The State’s revenue surplus at the end of April is significant, and likely to hold through the end of SFY 2026 in late June. That likelihood marks a substantial improvement in State finances relative to earlier this year. That improvement is largely due to the Tax Amnesty Program, but underlying revenue sources also seem to suggest the State’s revenue slide has reached bottom and is rebounding. However, such a rebound will depend on key factors, including the health of the broader national economy and specific trends like the desire of residents to participate in legal gambling, that are largely outside of State policymaker control.

Endnotes

[1] To learn more about the State’s General Fund and Education Trust Fund, see NHFPI’s New Hampshire Policy Points 2025 chapter about the State Budget and NHFPI’s February 2017 publication Building the Budget.

[2] Calculations based on the cash-basis receipts reported by the New Hampshire Department of Administrative Services in the Monthly Revenue Focus reports. The Statewide Education Property Tax revenues, which are only substantially shifted by policy changes as the tax is designed to collect the same amount of revenue each year, are excluded from these comparative analyses. For more information about the Statewide Education Property Tax, see NHFPI’s May 2021 analysis Statewide Education Property Tax Change Provides Less Targeted Relief and New Hampshire Policy Points 2025 edition chapter Funding Public Services.

[3] For more information on State revenue in SFY 2025 and how those revenues compared to SFYs 2023 and 2025, see page 6 of the New Hampshire Annual Comprehensive Financial Report for SFY 2025. To see the State Revenue Plan for each State fiscal year, as constructed based on revenue projections incorporated into the State Budget, visit the New Hampshire Department of Administrative Services webpage linking to State of New Hampshire Financial Reports.

[4] In this analysis, descriptions of April 2026 revenues or year-to-date revenues for SFY 2026 thus far are in reference to figures reported in the New Hampshire Department of Administrative Services Monthly Revenue Focus report for April SFY 2026.

[5] To learn the details of the Tax Amnesty Program, see the New Hampshire Department of Revenue Administration’s Technical Information Release TIR 2025-006 dated November 21, 2025.

[6] For more information, see NHFPI’s April 6, 2026 blog post Business Tax Receipts Dominate Tax Amnesty Program.

[7] Read more about February revenues in the New Hampshire Department of Administrative Services Monthly Revenue Focus report for February SFY 2026 and NHFPI’s March 9, 2026 analysis February Revenues Show Strong Final Push from Tax Amnesty Program and Adds to Surplus.

[8] To learn more about the Business Profits Tax and the Business Enterprise Tax, see NHFPI’s August 2023 Issue Brief State Business Tax Rate Reductions Led to Between $496 Million and $729 Million Less for Public Services and January 2026 Issue Brief Business Enterprise Tax Rate Decreases Have Lowered Revenue with Limited Economic Benefit. For a comparison of State tax revenue sources by relative collections, see slide 23 of NHFPI’s March 23, 2026 presentation The State Budget and Funding for Public Services in New Hampshire. To see comparisons of combined business tax revenues relative to the State Revenue Plan and over time, see page 6 of the New Hampshire Annual Comprehensive Financial Report for SFY 2025.

[9] See the New Hampshire Department of Administrative Services Monthly Revenue Focus report for March SFY 2026.

[10] Read more about the limit on credit carryforward in NHFPI’s January 10, 2025 blog State Revenue Deficit Widens After December Tax Receipts Fall Short.

[11] See the New Hampshire Department of Administrative Services Monthly Revenue Focus reports for refund comparisons.

[12] Learn more about the structure of business tax payment timing and references to the statutes establishing this structure in NHFPI’s May 2019 Issue Brief Funding the State Budget: Recent Trends in Business Taxes and Other Revenue Sources.

[13] These estimate, return, and extension data are provided directly by the New Hampshire Department of Revenue Administration at the end of every month. The month-end report distributed April 30, 2026 was used for this analysis.

[14] For more information, see NHFPI’s December 13, 2024 blog post November State Revenue Falls Behind Planned Levels Amid Declining Business Tax Receipts and Lower Interest Payments.

[15] To learn more about the Interest and Dividends Tax, see NHFPI’s January 2024 informational testimony NHFPI Testimony Related to the Interest and Dividends Tax.

[16] For more information, see the 2025 edition of New Hampshire Policy Point’s Funding Public Services chapter.

[17] See the New Hampshire Department of Administrative Services Revenue Plans by Fiscal Year webpage for more details.

[18] For more information on the relative importance of the Insurance Premium Tax in recent State revenue trends, see NHFPI’s September 2025 Issue Brief Shifting Sources: A Brief Look at Long-Term State Revenue Trends in New Hampshire.

[19] For more information, see the 2025 edition of New Hampshire Policy Point’s Funding Public Services chapter.

[20] For analysis of recent data about housing prices and supply in New Hampshire, see NHFPI’s March 30, 2026 Issue Brief High Prices and Low Supply Continue to Impact Housing Affordability in New Hampshire.

[21] For more information on gambling expansions, including Video Lottery Terminals, see NHFPI’s July 2016 column The Expanding Role of Gambling in State Finances, NHFPI’s July 2025 report The State Budget for Fiscal Years 2026 and 2027, and August 2025 blog The State Lottery Has Grown, Becoming More Important for Public Education.

[22] Figures used in this analysis are cash-basis reported numbers for April of each State fiscal year from the New Hampshire Department of Administrative Services Monthly Revenue Focus reports.

[23] Inflation adjustment completed using the U.S. Bureau of Labor Statistics Consumer Price Index-Urban in New England for all items.